Bryan Stiger, CFP®

Meet our writer

Bryan Stiger, CFP®

Financial Planner, Betterment

Bryan provides “big picture” financial planning advice to clients and is passionate about helping others with financial literacy. He holds a master’s degree in Finance and has been quoted in media outlets such as Business Insider and CNBC.

Articles by Bryan Stiger, CFP®

-

![]()

The Role Of Life Insurance In A Financial Plan

Life insurance helps loved ones cover expenses and progress toward financial goals after ...

The Role Of Life Insurance In A Financial Plan Life insurance helps loved ones cover expenses and progress toward financial goals after you’re gone. When you’re making a financial plan, life insurance probably isn’t the first thing that comes to mind. But if you pass away, life insurance helps take care of your loved ones when you can’t. It helps your beneficiaries stay on track to pay off your mortgage, pursue secondary education, retire on time, and reach the other financial goals you’ve made together. It protects them from the sudden loss of income they could experience. Life insurance won’t help you reach your goals, but it ensures that your loved ones still can when you’re gone. In this guide, we’ll cover: Life insurance basics How to decide if you need life insurance How to apply for life insurance Life insurance basics Whatever policy you buy, life insurance has five main components: Policyholder: The person or entity who owns the life insurance policy. Usually, this is the person whose life is insured, but it’s also possible to take out a policy on someone else. The policyholder is responsible for paying the monthly or annual insurance premiums. Insured: Also known as the life assured, this is the person whose life the policy covers. The cost of life insurance heavily depends on who it covers. Beneficiary: The person, people or institution(s) that receive money if the insured dies. There can be more than one beneficiary named on the policy. Premium: This is what you pay monthly or annually to keep a policy active (or “in-force”). Stop paying premiums, and you could lose coverage. Death benefit: This is what the insurance company pays the beneficiaries if the insured person passes away. As soon as the policy is in force, the beneficiaries are usually eligible for the death benefit. In some circumstances, insurance companies aren’t obligated to pay the death benefit. This includes when: The insured outlives the policy term The policy lapses or gets canceled The death occurs within two years of the policy being in-force and the insurance company finds evidence of fraud on the application Term life insurance vs. permanent life insurance Term life policies last for a set period of time. When the term is up, the policy expires. This is usually the most affordable type of life insurance. And since it’s not permanent, you can let it expire once you reach your financial goals and have other means of providing for your loved ones. You’re not stuck paying for protection you no longer need. In fact, the premiums are so low that you can even abandon your policy later without losing much money. Permanent life insurance policies don’t have an expiration date. They last for as long as the policyholder pays the premiums. Since they’re permanent, these policies also have a cash-value component that can be borrowed against. These policies have higher premiums than term policies. Permanent life insurance policies include whole, variable, universal and variable universal life. So, should you sign up for life insurance? If you have financial dependents, and you don’t have enough money set aside to provide for them in the event of your passing, then life insurance should be considered. Here are some cases where buying life insurance might not be beneficial: You have neither a spouse nor dependents You don’t have any debt You can self-insure (you have enough saved to cover debts and expenses) Unless that describes you, getting life insurance should probably be on your To-Do list. How much coverage do you need, though? That depends. If you’re married, you might want to leave a financial cushion for your spouse. You also might want to make sure that they can continue to pay off the loans you co-signed. For example, your spouse could lose your house if they are unable to keep up with the mortgage payments. Consider choosing a policy that will cover any debts your spouse may owe and the loss of your income. A common rule of thumb for an amount is 10x the insured's income. If you have kids, consider getting a policy big enough to cover all childcare costs, including everything you pay now and what you may pay in the future, such as college tuition. You may wish to leave enough behind for your spouse to cover your kids’ education expenses. Your death benefit should usually cover the entire amount of all these expenses, minus any assets you already have that your family can use to make up some of the financial shortfall. This could be as little as $250,000 or as much as several million dollars. How to apply for life insurance Applying for life insurance usually takes four to eight weeks, but you can often complete the process in just seven steps: Compare quotes from multiple companies Choose a policy Fill out an application Take a medical exam Complete a phone interview Wait for approval Sign your policy And just like that, you have life insurance—and your dependents have a little more peace of mind. Life insurance is about preparing for the unexpected. As you set financial goals and plan for the future, it’s important to consider what your family’s finances would look like without you. This is your fail-safe. In the worst case scenario, life insurance could prevent financial loss from adding to your loved ones’ grief. -

![]()

Putting Together An Estate Plan For Your Investments

Help make sure the right people make decisions on your behalf and receive the inheritance ...

Putting Together An Estate Plan For Your Investments Help make sure the right people make decisions on your behalf and receive the inheritance you want. If you suddenly found yourself on life support or developed a serious mental illness, what would happen to you? If you died tomorrow, what would happen to your children, and your things? State laws can answer these questions, or you can decide for yourself with an estate plan. By preparing in advance, you can help ensure that the right people make decisions on your behalf and that your loved ones receive the inheritance you want them to. (And if there’s anyone who shouldn’t receive an inheritance, your estate plan can keep them from cutting in.) In this guide, we’ll cover: What your estate plan needs to do Who should be part of your estate plan What documents to include in your estate plan An estate plan can define what will happen with the people and things you’re responsible for if you die or become incapacitated. Who will make medical or financial decisions on your behalf? Who will be your child’s new guardian? How will your finances be divided? Who gets the house? Those aren’t decisions you want a stranger to make for you. But without an estate plan, that could be what happens. Unless you say otherwise, state laws will govern your estate. And those generic laws may not align with your values and goals. That’s why whatever your age and whatever your financial situation, an estate plan is crucial. Before you start creating an estate plan, it helps to consider your unique situation. What does your estate plan need to do? Your estate plan can answer questions about what happens with your assets and how your loved ones will be taken care of when you’re gone. So you need to consider how you’d answer those questions now, anticipating choices that could come up in the future. For example, if you’re expecting to receive an inheritance, be sure to think through how your estate plan would distribute it or who would manage it. And if there’s anyone you need or want to financially support, that should guide your estate plan as well. Who should be part of your estate plan? An estate plan doesn’t just decide who gets what. It can also determine who’s in charge of what. There are several key roles to consider in your estate plan. You may want to divide these roles between multiple people, or let one call the shots. For example, if all of your children have the authority to make medical decisions on your behalf, that may lead to more thoughtful decisions. But it’s a trade off. Each of the people you give power to has to sign off on decisions, which can slow things down and make it much more difficult to coordinate. Financial Power Of Attorney (POA) Giving someone financial power of attorney can make it easier for them to pay bills, file taxes, or cash checks on your behalf. You can decide how broad or limited their control is. Even with broad authority, a financial power of attorney can’t change your will. The idea is that if you’re physically or mentally unable to take care of your day-to-day finances, you’ve designated someone to take care of that for you. Make sure the person you designate has a copy of this paperwork or knows where to find it. You can also give a copy to your financial institutions. Advanced Healthcare Directive An advanced healthcare directive helps decide how to handle medical decisions when you can’t make them yourself. It can lay out specific care instructions like, “Do not resuscitate,” but it can also give someone medical power of attorney to make decisions on your behalf. When you can’t think through important decisions anymore, who do you want to make the call? Your spouse? Your children? A parent? A sibling? As with financial power of attorney, you can define the scope of this power. Joint Owner If you name someone the joint owner of your accounts, then when you die, they become the sole owner. This is a common way for married couples to handle their estates, and it usually keeps the state from getting involved in distributing your assets when you die. Just keep in mind: anyone you name as a joint owner gains equal control of your assets while you’re alive, too. Also, retirement accounts such as 401(k)s and IRAs can’t be put into joint ownership. Beneficiaries You may also want individual assets to go to specific people. In that case, you may want to name beneficiaries for your bank accounts, investment accounts, life insurance policy, real estate, and other major assets. Name beneficiaries in your will, and these assets will have to go through probate first, where a court process proves that your will is authentic. This typically increases the time before your beneficiaries receive the inheritance and reduces the amount that ultimately makes it to them. For your accounts, adding beneficiaries can be as simple as filling out a form through your bank or investment firm. In some states, you may be able to use a Transfer on Death (TOD) Deed to ensure that your real estate goes directly to the beneficiary. What documents should your estate plan include? While there are many legal documents that make up an estate plan, two of the more important ones are a will and a trust. Here’s what those entail. Last will and testament A will serves several purposes. It can clearly lay out your final wishes, state who will take care of your non-adult children, and say who receives your belongings. If you do a good job naming beneficiaries for your assets, this mostly affects personal belongings. A will should usually start with a declaration. This identifies who you are and says that the document is your will. You’ll generally have to sign it in front of witnesses (and possibly a notary). You’ll need to choose an executor who will ensure your wishes are carried out, including any final arrangements for your death and funeral services. Your will can define the scope and limitations of their power as well as any compensation you want them to receive. If you have non-adult children, your will should name their new guardians. Wills also define bequests: individual gifts you give someone. Think family heirlooms. Clothing. Vehicles. Money. You can change your will at any time. And as your valuables and relationships change, you’ll want to keep it up to date. Trust A trust is a legal entity that gives someone (usually you) the right to hold your assets for the benefit of someone else. It provides several advantages that help your financial plan live on when you’re gone. Some types of trusts can shield your assets from estate taxes. They can also protect your assets from creditors, litigation, and even public records. As part of your trust, these assets also avoid probate. By using a trust, you keep greater control over your assets, too. You can define who gets your assets and when, as well as what they can do with them. With Betterment, you can open an account in the name of a trust–revocable or irrevocable–that you have already established. -

![]()

An Investor’s Guide To Diversification

Diversification is an investing strategy that helps reduce risk by allocating investments ...

An Investor’s Guide To Diversification Diversification is an investing strategy that helps reduce risk by allocating investments across various financial assets. Here’s everything you need to know. In 1 minute When you invest too heavily in a single asset, type of asset, or market, your portfolio is more exposed to the risks that come with it. That’s why investors diversify. Diversification means spreading your investments across multiple assets, asset classes, or markets. This aims to do two things: Limit your exposure to specific risks Make your performance more consistent As the market fluctuates, a diverse portfolio generally remains stable. Extreme losses from one asset have less impact—because that asset doesn’t represent your entire portfolio. Maintaining a diversified portfolio forces you to see each asset in relation to the others. Is this asset increasing your exposure to a particular risk? Are you leaning too heavily on one company, industry, asset class, or market? In 5 minutes In this guide, we’ll: Define diversification Explain the benefits of diversification Discuss the potential disadvantages of diversification What is diversification? Financial assets gain or lose value based on different factors. Stocks depend on companies’ performance. Bonds depend on the borrower’s (companies, governments, etc.) ability to pay back loans. Commodities depend on public goods. Real estate depends on property. Entire industries can rise or fall based on government activity. What’s good or bad for one asset may have no effect on another. If you only invest in stocks, your portfolio’s value completely depends on the performance of the companies you invest in. With bonds, changing interest rates or loan defaults could hurt you. And commodities are directly tied to supply and demand. Diversification works to spread your investments across a variety of assets and asset classes, so no single weakness becomes your fatal flaw. The more unrelated your assets, the more diverse your portfolio. So you might invest in some stocks. Some bonds. Some fund commodities. And then if one company has a bad quarterly report, gets negative press, or even goes bankrupt, it won’t tank your entire portfolio. You can make your portfolio more diverse by investing in different assets of the same type—like buying stocks from separate companies. Better yet: companies in separate industries. You can even invest internationally, since foreign markets can potentially be less affected by local downturns. What are the benefits of diversification? There are two main reasons to diversify your portfolio: It can help reduce risk It can provide more consistent performance Here’s how it works. Lower risk Each type of financial asset comes with its own risks. The more you invest in a particular asset, the more vulnerable you are to its risks. Put everything into bonds, for example? Better hope interest rates hold. Distributing your assets distributes your risk. With a diversified portfolio, there are more factors that can negatively affect your performance, but they affect a smaller percentage of your portfolio, so your overall risk is much lower. If 100% of your investments are in a single company and it goes under, your portfolio tanks. But if only 10% of your investments are in that company? The same problem just got a whole lot smaller. Consistent performance The more assets you invest in, the less impact each one has on your portfolio. If your assets are unrelated, their gains and losses depend on different factors, so their performance is unrelated, too. When one loses value, that loss is mitigated by the other assets. And since they’re unrelated, some of your other assets may even increase in value at the same time. Watch the value of a single stock or commodity over time, and you’ll see its value fluctuate significantly. But watch two unrelated stocks or commodities—or one of each—and their collective value fluctuates less. They can offset each other. Diversification can make your portfolio performance less volatile. The gains and losses are smaller, and more predictable. Potential disadvantages of diversification While the benefits are clear, diversification can have a couple drawbacks: It creates a ceiling on potential short-term gains Diverse portfolios may require more maintenance Limits short-term gains Diversification usually means saying goodbye to extremes. Reducing your risk also reduces your potential for extreme short-term gains. Investing heavily in a single asset can mean you’ll see bigger gains over a short period. For some, this is the thrill of investing. With the right research, the right stock, and the right timing, you can strike it rich. But that’s not how it usually goes. Diversification is about playing the long game. You’re trading the all-or-nothing outcomes you can get with a single asset for steady, moderate returns. May require more maintenance As you buy and sell financial assets, diversification requires you (or a broker) to consider how each change affects your portfolio’s diversity. If you sell all of one asset and re-invest in another you already have, you increase the overall risk of your portfolio. Maintaining a diversified portfolio adds another layer to the decision-making process. You have to think about each piece in relation to the whole. A robo advisor or broker can do this for you, but if you’re managing your own portfolio, diversification may take a little more work. -

![]()

How to Build an Emergency Fund

An emergency fund keeps you afloat when your regular income can’t. Learn how to start one ...

How to Build an Emergency Fund An emergency fund keeps you afloat when your regular income can’t. Learn how to start one and grow it. In 10 seconds An emergency fund keeps you afloat when your regular income can’t. Try saving at least three months’ worth of expenses, so your finances can handle a sudden job loss or medical emergency. In 1 minute An emergency fund helps protect you from the most common financial crises. It helps cover unexpected expenses that don’t fit into your regular budget, and buys time to find a new job or manage a transition. For most people, the goal is to have enough funds set aside to pay for at least three months of living expenses, including food, housing, and other essential costs. But exactly how much you need depends on your situation. If you have more dependents or greater risks, you may need more than that to feel comfortable. Ideally, you should automate deposits into your emergency fund to make sure it grows each month until it reaches an appropriate size. You may also want to put this money into a cash account or low-risk investment account to help it grow faster, as long as you are ok with taking on this risk. Betterment makes both of these options easy, and with recurring deposits, you can make steady progress toward your goal. In 5 minutes In this guide we’ll cover: Why you should build an emergency fund How much you should save How to grow your emergency fund You can’t anticipate every financial disaster. But with an emergency fund, you can reduce their impact on your life. It’s a special account you don’t touch until you absolutely need to. If you’re like most people, this is one of your first and most important financial goals. Without an emergency fund, you could find yourself taking on high-interest debt to avoid losing your home. Or unable to meet basic needs, you may have to make hard choices about which necessities to live without. So, how much should you save? What should you do with the money you set aside? And what counts as “an emergency”? Your emergency fund is personal. It needs to fit your life, your needs, and your risks. Some may only need a few thousand dollars. Others may need tens of thousands. It all depends on your regular expenses and how prepared you want to be. How large should your emergency fund be? For most people, the goal is to have enough to cover at least three months of expenses. That’s rent or mortgage, utilities, food, and anything else you pay every month. If you unexpectedly lost your job or had a medical crisis, your emergency fund should be enough to help you through most transitions. Some folks should save more. If you’re a single parent or the only person with income in your household, a sudden loss of income would have a greater impact. If you work in an industry with high turnover, or you have a serious medical condition, you’re more likely to need these funds, so you may want to save more, such as six months of your monthly expenses. It may help to think of your emergency fund as time. This isn’t just a target dollar amount. It’s months of time. How long would you like to keep the bills paid without a job? How much would it take to do that? That’s the amount you should save. There’s no magic number that’s right for every person. And since it’s based on your current cost of living, the amount you’ll want to save will change with your expenses. Live more frugally, and you may be more comfortable with a smaller emergency fund. Get a bigger house or apartment, add a family member, or spend more on basic needs, and you’ll need a bigger emergency fund. How to build an emergency fund The hardest part of building an emergency fund is figuring out how saving fits into your life. It helps to work backward from your goal. Once you know how much you need to save, decide when you want to save it by. The sooner the better, but choose a timeline that makes sense for you. Then break your goal into chunks—how much do you need to save each month or each paycheck to get there on time? The last part is easy. Make your savings automatic with recurring deposits. You make the commitment once, then see steady progress toward your goal. You don’t have to think about it anymore. Set up a Safety Net goal with Betterment, and we’ll take care of this for you. Set how much you want to save and when you want to save it by, then decide how much you can put toward that goal each month. Create a recurring deposit, and you’ll start saving automatically. This video sums it all up. Where should you put your emergency fund? A lot of people put their emergency fund in a savings account at a bank. It keeps their money liquid, and it’s federally insured by the FDIC. So there’s little risk of losing what you’ve saved. Obviously, you want your emergency fund to be there when you need it, so it’s understandable why so many people are drawn to savings accounts. But it may not be the best way to grow your fund, either. Most savings accounts generate so little interest that they’re basically cash. It’s a step above putting money under your mattress. And like cash, savings accounts will usually lose value over time due to inflation. Thankfully, you have options. You can generate more interest without taking on much more risk. Here are some alternative places to put your emergency fund. High Yield Cash Account Like a regular savings account, most cash accounts are federally insured. But unlike a traditional savings account, these can generate meaningful interest. A high yield account takes your money further, and it’s still highly liquid. Certificate of Deposit (CD) A certificate of deposit, or CD, is basically a short-term investment. It lasts for a fixed duration, such as 12 months or 5 years. At the end of this period, the CD “matures,” and you typically earn more interest than you would with a high yield cash account. CDs are federally insured and still low-risk, but until your CD matures, it’s not liquid unless you pay a penalty to get out of the CD early. This makes it a little riskier for an emergency fund, since you never know when you’ll find yourself in a crisis. Low-Risk Investment Account Investment accounts can offer greater growth potential in exchange for taking on more risk. While stocks are considered volatile because they frequently change in value, bonds are generally more stable. An investment portfolio consisting of all bonds can still outpace a CD, a high yield account, and inflation, while putting your emergency fund at significantly less risk when compared to a portfolio consisting entirely of stocks. If you feel investing is the right move for you, Betterment recommends giving yourself a bigger buffer, adding 30% to your target amount. That way your money can grow faster, but it’s also protected against potential losses. -

![]()

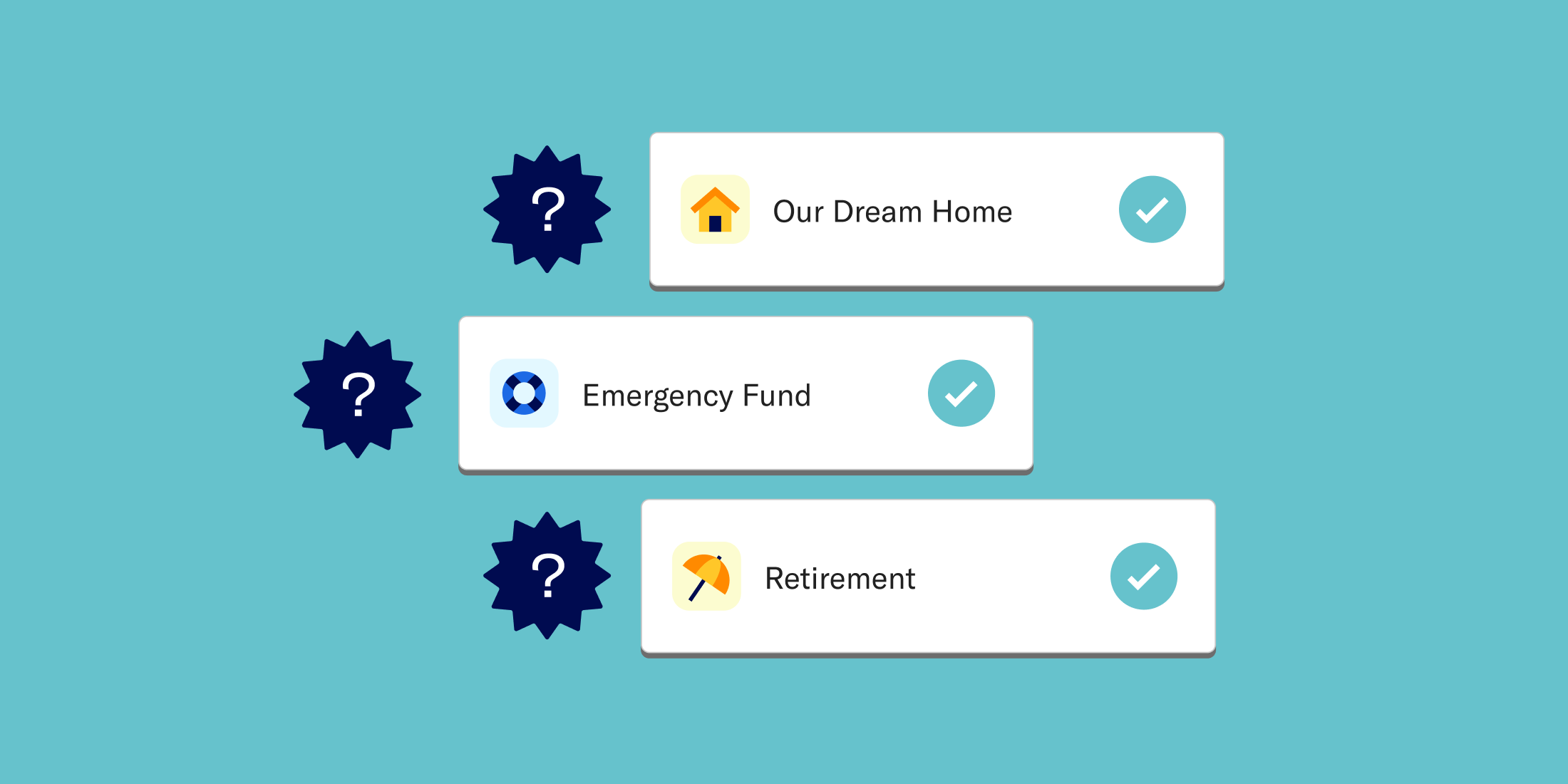

Setting and Prioritizing Your Financial Goals

When you have more than one, think in terms of importance, timeline, and the amount you ...

Setting and Prioritizing Your Financial Goals When you have more than one, think in terms of importance, timeline, and the amount you need In 1 minute Saving for big financial goals like retirement doesn’t have to mean letting go of your other goals. But prioritizing them is tough. How are you supposed to weigh something like a distant retirement versus a more immediate financial goal, like a honeymoon? Or a down payment on a home? Start by identifying all of the things you’d like to achieve. They might be big-ticket items you want to buy, experiences you want to have, or expenses you want to be prepared for. Once you’ve named them, estimate how much you’d need to reach each goal, and how soon you’d like to reach them. After you’ve clearly defined the goals you could save for, it’s time to choose which ones matter most to you. You might rank every goal or just narrow the list down to your top five to ten. Then you can calculate how much you’d have to save each month to reach these goals based on your timeline. From there, turn to your budget. Decide how much you can afford to save each month and apply it to your biggest goals first. We highly recommend turning on auto-deposit so you won’t be tempted to stop working toward your goals. Your financial goals don’t have to be set in stone, and neither does your plan. Over time, you may find that you can save more—or that you can’t save as much as you thought. Maybe it’ll take more or less to reach your goal. Or your priorities might change. That’s OK. With Betterment, it’s easy to set, automate, and adjust your goals. In 5 minutes In this guide, we’ll cover: Defining your financial goals Prioritizing your goals Deciding how to allocate your money Adjusting goals as needed Financial goals help you plan for the things you’d like to do with your money, but can’t afford to do right now. Like retiring. Buying a house. Sending your kids to college. Getting that dream car. Remodeling your kitchen. When you know what you want to do, you can estimate how much you need and when you need it. Knowing your goals also helps you choose the right financial accounts, so you can reach them sooner. But what happens when you have multiple financial goals? All of a sudden, it’s harder to know how much to put toward each goal. Thankfully, working toward one goal doesn’t mean you can’t reach another. Here’s how to set and prioritize your financial goals. Define your financial goals If you sit down and think about all of the things you’d like to do with your money, you can probably create a much longer list than you’d expect. Do it. It’s worth taking the time to write down every goal—because you might be forgetting something important! Some of your goals could be as simple as saving up for holiday gifts, as important as building a safety net, or as big as planning for retirement or long-term care. If it’s on your mind, put it on the list. Part of this process should involve estimating how much you’d need to save to reach each goal and when you’d like to reach it. Is it months away? Years? Decades? Will it take hundreds of dollars or hundreds of thousands? Each goal should have a timeline and amount. At Betterment, it’s easy to add this information every time you set up a goal. (And you can change it at any time.) Prioritize what matters to you Your financial goals are yours. This isn’t about what your parents want or what your friends expect from you. Whatever your goals are, prioritize them based on how important they are to you. Remember that ranking your goals doesn’t mean you won’t reach the ones on the bottom. For example, you shouldn’t be afraid to pay down debt and invest at the same time. This is just to help you think about which goals you care about the most. Once you’ve ranked your goals, your list might look like this: Pay off medical debt Build emergency fund Save for retirement Put a down payment on a house Remodel the bathroom You can include as many goals as you want. And in Betterment, you can add each goal to your account, whether you put anything toward it or not. Apply your budget to your list Now that you know how much you need to save, when you need to save it by, and which goals are most important to you, it’s time to see what you can actually accomplish. Using your estimated amount and your timeline (in investing, this is called your “time horizon”), calculate how much you need to save each month to reach each goal. It’s OK if this is more than you can afford to save right now. Putting the numbers in front of you with an ordered list helps you ask questions like, “Can I reach all of these goals on these timelines?” and “Which goal(s) am I willing to delay in order to make progress on the others? If you plan on investing to reach your goal, you should also consider how much you can expect to earn toward these goals with an investment account. Every time you set up a goal in Betterment, we’ll handle this part for you. You can see how achievable your goal is based on how much you put toward it. Automate your financial goals The best way to make sure you reach your goals? Automate them. Don’t make the mistake of putting your goals on pause. Set up recurring deposits for each goal with the amount you’ve set aside for them, and the right amount automatically goes to the right goal. This makes it easy to budget around your goals, and you won’t accidentally miss a month. The strategy is often called “paying yourself first” because you’re putting money toward your highest priorities before spending it on anything else. Want to start working toward your financial goals? Set up a goal with Betterment, and see what you can achieve.