My 401(k). My future.

Use the resources below to make the most of your 401(k) plan and strengthen your financial wellness.

Featured

Most Recent Posts

-

What is the maximum 401(k) contribution?

What is the maximum 401(k) contribution? Everything you should know to help your employees save smarter this year. Every year, the IRS updates the rules governing 401(k) and IRA contributions, and they recently announced the guidelines for 2022. So what are the updates for 2022? Here’s the big news: The contribution limit for employer-sponsored 401(k) plans is $20,500 for individuals under age 50, up from $19,500. This is the first time the limit has gone up in two years! Now, let’s get into the details. In this article, we’ll discuss the new 2022 limits and rules—and how they may impact your retirement goals. What you need to know about retirement plans (and their contribution rules) As you may know, there are two primary retirement plans: employer-sponsored retirement plans and IRAs. Here’s how they differ: Employer-sponsored plans—like 401(k), 403(b), and 457 plans—are only available if the employer offers one. If they’re eligible, individuals can contribute to both an employer-sponsored plan and an IRA. IRAs are tax-deferred or tax-advantaged retirement accounts that individuals (who qualify) can open up on their own—regardless of their employment situation. Because the IRS offers tax advantages to people who participate in these plans, there are naturally a few strings attached. Specifically, individuals can only contribute a certain amount of money in a given year—and that amount decreases if they earn above a certain threshold. Good news—Most people can contribute more in 2022. If your employees ask “what is the 401(k) limit for 2022?” you’ll be able to share the good news that most people can contribute up to $20,500 in 2022. This is up from $19,500, which was the limit in 2020 and 2021. When you look at the following contribution limits, you’ll notice that some of them take into consideration taxable income, which impacts how much highly compensated employees and low-income earners can save. Estimating taxable income can be complicated, and since Betterment is not a tax advisor, we suggest talking with a qualified tax professional. Let’s take a closer look at the 2022 contribution limits. 1. Employer-sponsored Plan Contribution Limits In 2022, the limit on annual contributions to Roth or Traditional 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plans increases to $20,500. The additional catch-up contribution limit remains unchanged at $6,500 for a total contribution limit of $27,000 for employees 50 years old and older. 2. IRA Contribution Limits In 2022, the limit on annual contributions to an IRA is unchanged at $6,000. The additional catch-up contribution limit for individuals 50 years old and over remains at $1,000. The total contribution limit is $7,000 for employees 50 years old and older. Retirement Account Contribution Limits Contribution Limits Catch-up Contribution Limit (for individuals age 50 and above) Account Type 2021 2022 2021 2022 Traditional IRA Roth IRA $6,000 $6,000 $1,000 $1,000 401(k) 403(b) 457 Plans $19,500 $20,500 $6,500 $6,500 Income Limits for Deductible Traditional IRA Contributions One of the best benefits of a Traditional IRA is that you can deduct contributions on your tax return. However, if you or your spouse are covered by an employer-sponsored retirement plan, Traditional IRA contributions are only deductible if your modified adjusted gross income (MAGI) falls below a certain threshold. Above that threshold, there’s a “phase-out” range in which an individual is eligible for a partial deduction, and after that range, contributions are not deductible. Traditional IRA Deductibility Limits for Individuals with an Employer-sponsored Plan 2021 2022 Filing Status Income (MAGI) Income (MAGI) Deduction Limit Single individuals ≤ $66,000 ≤ $68,000 Full deduction up to the contribution limit $66,000 – $76,000 $68,000 – $78,000 Partial deduction ≥ $76,000 ≥ $78,000 No deduction Married, filing jointly ≤ $105,000 ≤ $109,000 Full deduction up to the contribution limit $105,000 – $125,000 $109,000 – $129,000 Partial deduction ≥ $125,000 ≥ $129,000 No deduction Married, filing separately < $10,000 < $10,000 Partial deduction ≥ $10,000 ≥ $10,000 No deduction Traditional IRA Deductibility Limits for Individuals without an Employer-sponsored Plan 2021 2022 Filing Status Income (MAGI) Income (MAGI) Deduction Limit Single individuals All incomes All incomes Full deduction up to the contribution limit Married, filing jointly + neither individual or spouse has an employer-sponsored plan All incomes All incomes Full deduction up to the contribution limit Married, filing jointly + spouse has an employer-sponsored plan ≤ $198,000 ≤ $204,000 Full deduction up to the contribution limit $198,000 – $208,000 $204,000 – $214,000 Partial deduction ≥ $208,000 ≥ $214,000 No deduction Married, filing separately < $10,000 < $10,000 Partial deduction ≥ $10,000 ≥ $10,000 No deduction 3. Income Limits for Roth IRA Contributions To read more about the IRA deduction limits, refer to details available from the IRS. Roth IRA contributions are not tax deductible. However, qualifying withdrawals (typically in retirement) can be made on a tax-free basis. However, to make the maximum $6,000 Roth IRA contribution, an individual’s income must fall below a certain threshold. In 2022, eligibility to contribute to a Roth IRA starts to phase out at $129,000 for single filers and $204,000 for married couples (filing jointly). That’s a higher start of the phase out threshold than in 2021, which began at $125,000 for single individuals and $198,000 for married couples. 4. Income Ranges for Partial Roth IRA Eligibility Individuals whose incomes fall within the following ranges are limited to making partial Roth IRA contributions. Those whose incomes fall below these ranges can contribute the full amount. Individuals with incomes above the range cannot contribute to a Roth IRA that year. Income Tax Filing Status 2021 MAGI 2022 MAGI Single $125,000 – $140,000 $129,000 – $144,000 Married Filing Jointly $198,000 – $208,000 $204,000 – $214,000 If you are married and file separately and lived with your spouse at any point during the year, you will be completely phased out of making Roth IRA contributions if your MAGI is $10,000 or more. For more information and guidance regarding Roth IRAs, review the expanded IRS rules. Income Limits for the Retirement Savings Contributions Credit (Saver’s Credit) To help low-income people save for retirement, the IRS offers the “Saver’s Credit.” Individuals may be eligible for the credit if they’re saving for retirement and their income falls below specific ranges. This credit offsets the individual’s income-tax liability; however, it phases out as the individual’s adjusted gross income (AGI) increases.

-

How to pick a 401(k) contribution rate

How to pick a 401(k) contribution rate Your 401(k) contribution rate - also known as a deferral rate or savings rate - is a key part of a successful retirement strategy. You’ve taken that first step and have set up your Betterment 401(k) account - well done! One important piece to consider next is your contribution rate - how much from each paycheck will go into your account? With your Betterment 401(k), you could use a percentage or a fixed dollar amount, whichever you prefer. Here are a few things to consider: Were you automatically enrolled? Many employers choose to automatically enroll their employees in the plan with a default contribution rate of 3% – if you're not sure, please check with your employer or take a look in your Retirement goal. Keep in mind, whatever the default contribution rate is, it’s just a starting point. You can (and probably should) increase that contribution rate at any time in your account. At least a decade without a paycheck Most experts recommend contributing 10%–15% of your paycheck to have enough to last you through retirement - which could be 20-30 years considering how long people are living! If you retire at age 65, with a healthy lifestyle and no major risk factors, you could live well into your 80s or 90s. That means you'll want to set yourself up for living off your personal savings and investments for about 20 years! Starting small is better than nothing If 10-15% of your paycheck sounds absurd to you right now - deep breath, think of that as something to aim for. You can start with something smaller, maybe 5 or 6%, and slowly but surely increase your savings rate every year – your birthday? Give yourself a gift and increase it by 1%. Your work anniversary? Cheers to you, bump it up again. And those 1% increases can actually be a big deal. Go for the max Because of its tax benefits, the IRS sets a limit on how much you can put into your 401(k) every year. So you could aim to contribute as much as the IRS allows! For people 50 and over, the limit is higher, which is referred to as “catch-up contributions.” And if you really want to be an over-achiever, you can also contribute to an IRA, an individual retirement account, to save even more. Tax considerations With your Betterment 401(k), you can make contributions into a traditional 401(k) account and/or a Roth 401(k). There are tax benefits to both: Traditional 401(k): Contributions are deducted from your paycheck before taxes are withheld, which can lower your taxable income. Both your contributions and investment earnings are “tax-deferred,” meaning you won’t pay taxes on what you contributed to the account as well as any earnings until you withdraw the money at retirement. In other words, save on taxes now, pay taxes later. Roth 401(k): Contributions are made with after-tax dollars so your withdrawals—both the contributions and earnings—are tax-free once you decide to retire (minimum age, 59½), and as long as you’ve held the Roth account for at least five years. In other words, pay taxes now, no taxes later. Remember that you can use both! Say you want to contribute 10% towards your retirement? You can put 5% into a traditional 401(k) and 5% into the Roth 401(k). This is one way you can balance your tax exposure. If you already have your account set up, log in today to adjust your contribution rate or reassess your traditional and Roth contributions. Haven’t started saving in your Betterment 401(k) yet? Check your email for an access link from Betterment, or get in touch: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET

-

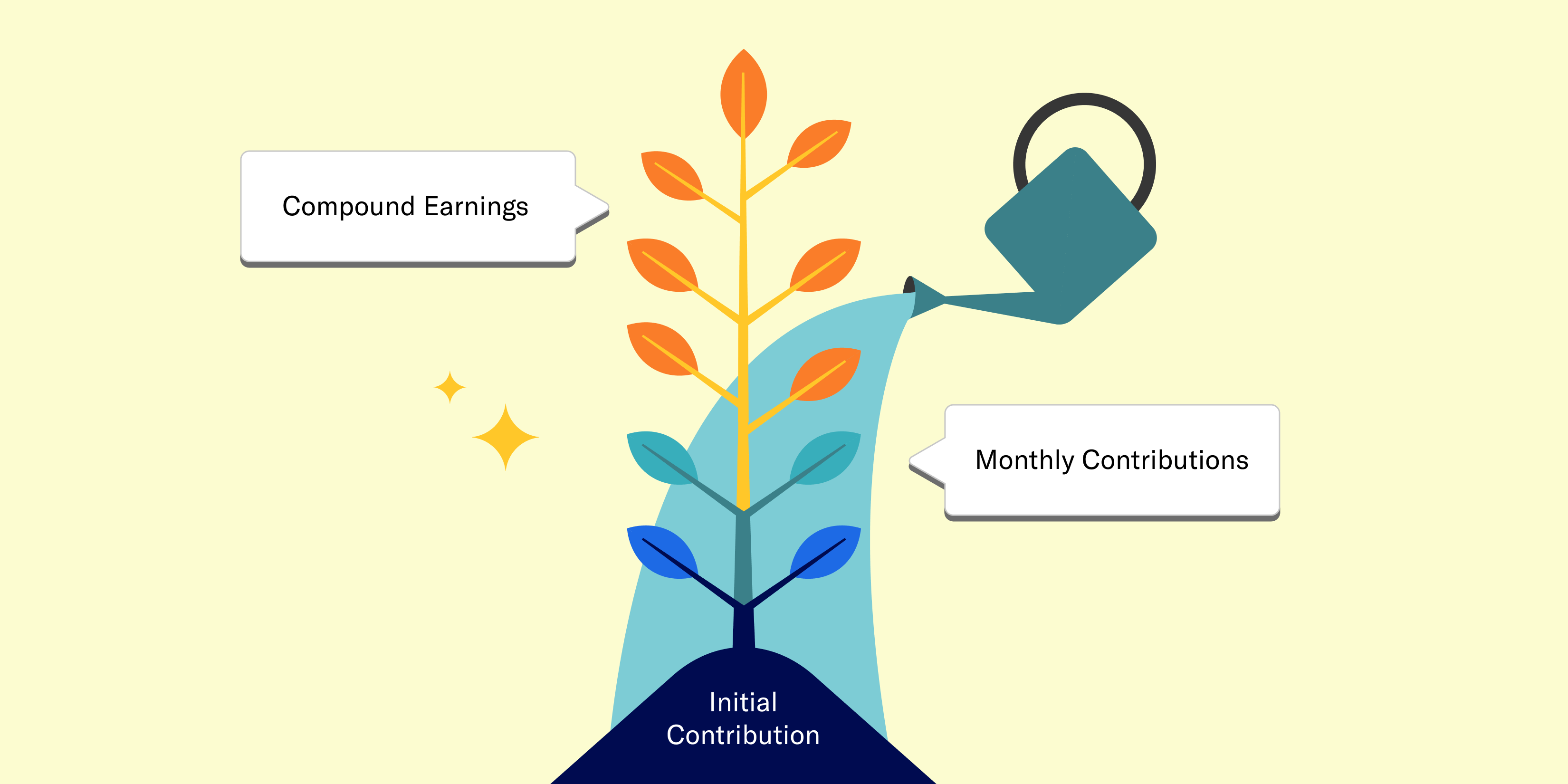

When’s the best time to invest for retirement? Now.

When’s the best time to invest for retirement? Now. Should you start saving for retirement? Unless you are on one of those richest-people-in-the-world lists - then the answer is, most likely, yes. From paying the rent or mortgage, credit card bills, student loans, daily living expenses - there are a lot of things competing for your money’s attention! The idea of saving for retirement can easily be pushed to the backburner for all of those other - completely understandable! - reasons. But we’re here to say - hold the phone. Even a little bit into a 401(k) can make a huge difference for your retirement. Rock and roll When a rock rolls down a hill, it goes faster and faster on its way down. It has something to do with momentum and physics – we’re not scientists here, we’re investment professionals. But the same concept applies to your 401(k) - not because of physics, but because of compounding interest. Compounding interest means that not only are your original dollars growing based on potential stock market gains, but that newly earned money also grows whenever the stock market goes up! See how it works with this calculator tool. Give compounding time to shine If the magic of compounding interest isn’t enough to get you going right away, there is one other factor to consider. If someone starts saving 6% of their paycheck at age 25, they are expected to end up with more money at age 65 than someone who contributes 10% starting at age 40. And here’s the real kicker - the person who’s doing 10% starting at age 40 will put in more of their own dollars, and is still expected to end up with less by the time they reach age 65. How is that possible? The 6% contributions had more time to grow – more time to roll down that hill gathering speed – or in this case – money. If you already have an account, log in today to view your contribution rate and consider giving it a bump – even a 1% increase can make a difference in your retirement years! Haven’t started saving in your Betterment 401(k) yet? Check your email for an access link from Betterment, or get in touch: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET

Explore our article library

Getting started

-

![]()

Rolling over is more than a dog trick

Rolling over is more than a dog trick Three reasons why rolling over 401(k)s from former employers may make sense. Have money sitting in 401(k) accounts from former employers? If so, you’re not alone. Recent research estimates that there are more than 24 million “forgotten” 401(k) accounts, holding approximately $1.35 trillion dollars. Are any of those dollars yours? If so, you should consider rolling any old 401(k) into your new Betterment 401(k) – here’s why: 1. Get a comprehensive view of your retirement savings When you have accounts here, there and anywhere, it’s hard to get a handle on where you stand. By rolling them over to your Betterment account and consolidating your retirement assets in one place, you can ensure your portfolio is appropriately diversified, monitor your progress, and rest assured that your investments aren’t competing or canceling each other out. 2. Avoid fees! Every 401(k) plan comes with fees. If you have multiple 401(k)s, you are paying fees for all of those accounts! Betterment has fees too –but we use low-cost exchange-traded funds (ETFs) in our portfolios, helping to keep fees low. 3. Access personalized financial advice and service Whether you want to talk investment strategy or review your retirement account, Betterment has CERTIFIED FINANCIAL PLANNER™ professionals and a customer support team that’s easy to reach when you need them. Your plan may include complimentary access to our team of CFPs® or you can book a call for a one-time fee. Other options Since you have access to a Betterment 401(k) through your employer, it could make sense for you to roll old 401(k)s into your Betterment 401(k) for all the reasons outlined above. But you do have other options: Leave it where it is. Roll it into an IRA (Individual Retirement Account), either with Betterment or another financial institution. Cash it out – this will come with taxes and potentially fees, and your money will no longer be invested (and potentially growing) for your retirement. Ready to roll? In just a few clicks, you can start the rollover process to Betterment and be set up with an appropriate investment strategy for you. You’ll receive a personalized set of rollover instructions via email, with no paperwork required by us. Have a different kind of account to roll over? No problem. You can roll over your IRAs, pensions, 401(a)s, 457(b)s, profit sharing plans, stock plans, and Thrift Savings Plans (TSPs) to Betterment using the same simple process. If you've already claimed your account, you can click here to start your rollover. If you have any questions along the way, our team is ready to help: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET -

![]()

When’s the best time to invest for retirement? Now.

When’s the best time to invest for retirement? Now. Should you start saving for retirement? Unless you are on one of those richest-people-in-the-world lists - then the answer is, most likely, yes. From paying the rent or mortgage, credit card bills, student loans, daily living expenses - there are a lot of things competing for your money’s attention! The idea of saving for retirement can easily be pushed to the backburner for all of those other - completely understandable! - reasons. But we’re here to say - hold the phone. Even a little bit into a 401(k) can make a huge difference for your retirement. Rock and roll When a rock rolls down a hill, it goes faster and faster on its way down. It has something to do with momentum and physics – we’re not scientists here, we’re investment professionals. But the same concept applies to your 401(k) - not because of physics, but because of compounding interest. Compounding interest means that not only are your original dollars growing based on potential stock market gains, but that newly earned money also grows whenever the stock market goes up! See how it works with this calculator tool. Give compounding time to shine If the magic of compounding interest isn’t enough to get you going right away, there is one other factor to consider. If someone starts saving 6% of their paycheck at age 25, they are expected to end up with more money at age 65 than someone who contributes 10% starting at age 40. And here’s the real kicker - the person who’s doing 10% starting at age 40 will put in more of their own dollars, and is still expected to end up with less by the time they reach age 65. How is that possible? The 6% contributions had more time to grow – more time to roll down that hill gathering speed – or in this case – money. If you already have an account, log in today to view your contribution rate and consider giving it a bump – even a 1% increase can make a difference in your retirement years! Haven’t started saving in your Betterment 401(k) yet? Check your email for an access link from Betterment, or get in touch: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET -

![]()

How to pick a 401(k) contribution rate

How to pick a 401(k) contribution rate Your 401(k) contribution rate - also known as a deferral rate or savings rate - is a key part of a successful retirement strategy. You’ve taken that first step and have set up your Betterment 401(k) account - well done! One important piece to consider next is your contribution rate - how much from each paycheck will go into your account? With your Betterment 401(k), you could use a percentage or a fixed dollar amount, whichever you prefer. Here are a few things to consider: Were you automatically enrolled? Many employers choose to automatically enroll their employees in the plan with a default contribution rate of 3% – if you're not sure, please check with your employer or take a look in your Retirement goal. Keep in mind, whatever the default contribution rate is, it’s just a starting point. You can (and probably should) increase that contribution rate at any time in your account. At least a decade without a paycheck Most experts recommend contributing 10%–15% of your paycheck to have enough to last you through retirement - which could be 20-30 years considering how long people are living! If you retire at age 65, with a healthy lifestyle and no major risk factors, you could live well into your 80s or 90s. That means you'll want to set yourself up for living off your personal savings and investments for about 20 years! Starting small is better than nothing If 10-15% of your paycheck sounds absurd to you right now - deep breath, think of that as something to aim for. You can start with something smaller, maybe 5 or 6%, and slowly but surely increase your savings rate every year – your birthday? Give yourself a gift and increase it by 1%. Your work anniversary? Cheers to you, bump it up again. And those 1% increases can actually be a big deal. Go for the max Because of its tax benefits, the IRS sets a limit on how much you can put into your 401(k) every year. So you could aim to contribute as much as the IRS allows! For people 50 and over, the limit is higher, which is referred to as “catch-up contributions.” And if you really want to be an over-achiever, you can also contribute to an IRA, an individual retirement account, to save even more. Tax considerations With your Betterment 401(k), you can make contributions into a traditional 401(k) account and/or a Roth 401(k). There are tax benefits to both: Traditional 401(k): Contributions are deducted from your paycheck before taxes are withheld, which can lower your taxable income. Both your contributions and investment earnings are “tax-deferred,” meaning you won’t pay taxes on what you contributed to the account as well as any earnings until you withdraw the money at retirement. In other words, save on taxes now, pay taxes later. Roth 401(k): Contributions are made with after-tax dollars so your withdrawals—both the contributions and earnings—are tax-free once you decide to retire (minimum age, 59½), and as long as you’ve held the Roth account for at least five years. In other words, pay taxes now, no taxes later. Remember that you can use both! Say you want to contribute 10% towards your retirement? You can put 5% into a traditional 401(k) and 5% into the Roth 401(k). This is one way you can balance your tax exposure. If you already have your account set up, log in today to adjust your contribution rate or reassess your traditional and Roth contributions. Haven’t started saving in your Betterment 401(k) yet? Check your email for an access link from Betterment, or get in touch: Send us an email: support@betterment.com Give us a call: (718) 400-6898, Monday through Friday, 9:00am-6:00pm ET

Investing with Betterment

Next-level planning

-

![]()

What is the maximum 401(k) contribution?

What is the maximum 401(k) contribution? Everything you should know to help your employees save smarter this year. Every year, the IRS updates the rules governing 401(k) and IRA contributions, and they recently announced the guidelines for 2022. So what are the updates for 2022? Here’s the big news: The contribution limit for employer-sponsored 401(k) plans is $20,500 for individuals under age 50, up from $19,500. This is the first time the limit has gone up in two years! Now, let’s get into the details. In this article, we’ll discuss the new 2022 limits and rules—and how they may impact your retirement goals. What you need to know about retirement plans (and their contribution rules) As you may know, there are two primary retirement plans: employer-sponsored retirement plans and IRAs. Here’s how they differ: Employer-sponsored plans—like 401(k), 403(b), and 457 plans—are only available if the employer offers one. If they’re eligible, individuals can contribute to both an employer-sponsored plan and an IRA. IRAs are tax-deferred or tax-advantaged retirement accounts that individuals (who qualify) can open up on their own—regardless of their employment situation. Because the IRS offers tax advantages to people who participate in these plans, there are naturally a few strings attached. Specifically, individuals can only contribute a certain amount of money in a given year—and that amount decreases if they earn above a certain threshold. Good news—Most people can contribute more in 2022. If your employees ask “what is the 401(k) limit for 2022?” you’ll be able to share the good news that most people can contribute up to $20,500 in 2022. This is up from $19,500, which was the limit in 2020 and 2021. When you look at the following contribution limits, you’ll notice that some of them take into consideration taxable income, which impacts how much highly compensated employees and low-income earners can save. Estimating taxable income can be complicated, and since Betterment is not a tax advisor, we suggest talking with a qualified tax professional. Let’s take a closer look at the 2022 contribution limits. 1. Employer-sponsored Plan Contribution Limits In 2022, the limit on annual contributions to Roth or Traditional 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plans increases to $20,500. The additional catch-up contribution limit remains unchanged at $6,500 for a total contribution limit of $27,000 for employees 50 years old and older. 2. IRA Contribution Limits In 2022, the limit on annual contributions to an IRA is unchanged at $6,000. The additional catch-up contribution limit for individuals 50 years old and over remains at $1,000. The total contribution limit is $7,000 for employees 50 years old and older. Retirement Account Contribution Limits Contribution Limits Catch-up Contribution Limit (for individuals age 50 and above) Account Type 2021 2022 2021 2022 Traditional IRA Roth IRA $6,000 $6,000 $1,000 $1,000 401(k) 403(b) 457 Plans $19,500 $20,500 $6,500 $6,500 Income Limits for Deductible Traditional IRA Contributions One of the best benefits of a Traditional IRA is that you can deduct contributions on your tax return. However, if you or your spouse are covered by an employer-sponsored retirement plan, Traditional IRA contributions are only deductible if your modified adjusted gross income (MAGI) falls below a certain threshold. Above that threshold, there’s a “phase-out” range in which an individual is eligible for a partial deduction, and after that range, contributions are not deductible. Traditional IRA Deductibility Limits for Individuals with an Employer-sponsored Plan 2021 2022 Filing Status Income (MAGI) Income (MAGI) Deduction Limit Single individuals ≤ $66,000 ≤ $68,000 Full deduction up to the contribution limit $66,000 – $76,000 $68,000 – $78,000 Partial deduction ≥ $76,000 ≥ $78,000 No deduction Married, filing jointly ≤ $105,000 ≤ $109,000 Full deduction up to the contribution limit $105,000 – $125,000 $109,000 – $129,000 Partial deduction ≥ $125,000 ≥ $129,000 No deduction Married, filing separately < $10,000 < $10,000 Partial deduction ≥ $10,000 ≥ $10,000 No deduction Traditional IRA Deductibility Limits for Individuals without an Employer-sponsored Plan 2021 2022 Filing Status Income (MAGI) Income (MAGI) Deduction Limit Single individuals All incomes All incomes Full deduction up to the contribution limit Married, filing jointly + neither individual or spouse has an employer-sponsored plan All incomes All incomes Full deduction up to the contribution limit Married, filing jointly + spouse has an employer-sponsored plan ≤ $198,000 ≤ $204,000 Full deduction up to the contribution limit $198,000 – $208,000 $204,000 – $214,000 Partial deduction ≥ $208,000 ≥ $214,000 No deduction Married, filing separately < $10,000 < $10,000 Partial deduction ≥ $10,000 ≥ $10,000 No deduction 3. Income Limits for Roth IRA Contributions To read more about the IRA deduction limits, refer to details available from the IRS. Roth IRA contributions are not tax deductible. However, qualifying withdrawals (typically in retirement) can be made on a tax-free basis. However, to make the maximum $6,000 Roth IRA contribution, an individual’s income must fall below a certain threshold. In 2022, eligibility to contribute to a Roth IRA starts to phase out at $129,000 for single filers and $204,000 for married couples (filing jointly). That’s a higher start of the phase out threshold than in 2021, which began at $125,000 for single individuals and $198,000 for married couples. 4. Income Ranges for Partial Roth IRA Eligibility Individuals whose incomes fall within the following ranges are limited to making partial Roth IRA contributions. Those whose incomes fall below these ranges can contribute the full amount. Individuals with incomes above the range cannot contribute to a Roth IRA that year. Income Tax Filing Status 2021 MAGI 2022 MAGI Single $125,000 – $140,000 $129,000 – $144,000 Married Filing Jointly $198,000 – $208,000 $204,000 – $214,000 If you are married and file separately and lived with your spouse at any point during the year, you will be completely phased out of making Roth IRA contributions if your MAGI is $10,000 or more. For more information and guidance regarding Roth IRAs, review the expanded IRS rules. Income Limits for the Retirement Savings Contributions Credit (Saver’s Credit) To help low-income people save for retirement, the IRS offers the “Saver’s Credit.” Individuals may be eligible for the credit if they’re saving for retirement and their income falls below specific ranges. This credit offsets the individual’s income-tax liability; however, it phases out as the individual’s adjusted gross income (AGI) increases. -

![]()

Traditional and Roth 401(k)s

Traditional and Roth 401(k)s Not sure what the difference is between traditional and Roth contributions for your 401(k)? We’ll explain. Ever hear the terms traditional 401(k) and Roth 401(k) thrown around and wonder – what are they? Should I be using them? Are these the keys to untold levels of wealth and financial security?! Easy does it. There are no secret weapons or silver bullets for securing a financially fit future. That said, traditional 401(k)s and Roth 401(k)s can be important tools when building your retirement strategy, so let’s make sure you know what they are. And a fun fact to know right away: you can use both. What do they have in common? A traditional 401(k) and Roth 401(k) are tax-advantaged accounts that allow you to save and invest for retirement (the tax advantages given to these types of accounts are not available in many other investing accounts). They’re available to you as a workplace benefit offered by your employer, and they’re funded with contributions from your paycheck – you set the amount, either as a dollar or a percent. The idea behind both is that they make it easier to save and invest for retirement automatically, like a built-in part of your budget. So what’s the difference? The difference is in how they are tax-advantaged. Traditional 401(k) contributions are made with pre-tax dollars, while Roth 401(k) contributions are made with after-tax dollars. Here’s an example. Let’s say you earn $40,000 a year and make contributions into a traditional 401(k). The contributions go into the account before your paycheck is taxed (“pre-tax”), lowering your taxable income. So if you save $3,000 throughout the year, you’d be paying taxes on $37,000 rather than $40,000. In addition, the money that you contribute—and any earnings—grow tax deferred until you withdraw it in retirement. At that time, your withdrawals are considered ordinary income and you’ll pay federal and possibly state taxes depending upon where you live. And, if you want to withdraw money before you turn age 59 ½, you’ll also be subject to a 10% penalty unless you qualify for an exception. If you decide to contribute to a Roth 401(k), the money is deducted from your paycheck after taxes have been taken out. So your paycheck is taxed now, reflecting your full salary of $40,000, which includes the contributions into the Roth 401(k) account. Roth 401(k) tax benefits come into play when you withdraw the money at retirement. Because you already paid taxes, you can withdraw contributions—and any earnings—tax-free if you’re age 59 ½ or older and have held your Roth 401(k) account for at least five years. Short answer: Traditional 401(k)s can lower your taxes now, but you’ll likely pay taxes when you withdraw the money at retirement. Roth 401(k)s don’t save you on taxes today, but you likely won’t have to pay taxes when you withdraw the money at retirement. Which type of account should I use? It ultimately depends on your unique financial situation and retirement goals. Betterment is not a tax advisor, and we encourage you to consult one if you want help reviewing your finances and goals. As a general rule: If you expect to be in a lower tax bracket in retirement, consider contributing pre-tax dollars into a traditional 401(k) account now, and you’ll pay taxes later. If you expect to be in a higher tax bracket in retirement, consider contributing after-tax dollars into a Roth 401(k) account, and pay your taxes now. What if I’m not sure if my tax bracket will be higher or lower in the future? You’re definitely not alone! In which case, it may make sense to invest in both. You’re allowed to make contributions to both types of accounts, spreading your tax exposure around. 5% in a traditional 401(k) and 5% in a Roth 401(k) would give you a 10% total contribution rate (in line with what many experts recommend). What if I want to withdraw my money early—that is, before I turn age 59 ½? Let’s start with the Roth 401(k). Because you already paid taxes on your contributions, you can generally withdraw that portion of the money tax-free. The portion of the withdrawal that represents your contributions to the account will generally be not taxed (and not subject to the 10% penalty). The portion of the withdrawal that represents earnings will be taxable and potentially subject to the 10% penalty. Most early withdrawals from a traditional 401(k) are taxed as ordinary income plus a 10% penalty. There are some exceptions, such as permanent disability. The tax advantages and ramifications of retirement accounts can be complicated. As Betterment is not a tax advisor, we encourage you to consult one to help you make this important decision. One more fun fact - former U.S. Senator from Delaware, William Roth, is the father of after-tax retirement accounts. Enjoy sharing that little bit of trivia at your next cocktail party, on us.