401K Plan Setup

Featured articles

-

![]()

Safe Harbor vs. Traditional 401(k) Plan: Which Is Right for You and Your Employees?

Weigh the pros and cons of each carefully before making a decision for your company.

Safe Harbor vs. Traditional 401(k) Plan: Which Is Right for You and Your Employees? Weigh the pros and cons of each carefully before making a decision for your company. 401(k) lingo can seem funny at first glance. There's "MEPs" and "PEPs," “QDIAs” and "Safe Harbors." And don't even get us started on "QACAs." But for now, let's linger on Safe Harbor 401(k) plans. If you’ve concluded that a 401(k) is right for your company, the next decision you face is what kind of 401(k) plan. They come in two primary flavors, with the Safe Harbor variety providing an alternative to the Traditional 401(k) plan. Does the “Safe Harbor” name mean the traditional route is riskier? Not necessarily. There's a host of pros and cons to each plan type. The best fit for your company depends ultimately on your unique situation. Keep reading to try on a Safe Harbor for size. Editor’s note: If you’re reading this during the first half of the year, with eyes on possibly implementing a Safe Harbor plan the following year, time is of the essence! Learn more about Safe Harbor setup deadlines below. Table of contents Safe Harbor 401(k) plans in a nutshell How nondiscrimination testing can trip up small businesses Safe Harbor may make sense for you if … Safe Harbor setup deadlines What Betterment at Work brings to your Safe Harbor 401(k) setup Safe Harbor 401(k) plans in a nutshell Safe Harbor plans offer companies an enticing deal. Contribute to your employees’ 401(k)s, the federal government says, and we’ll give you a free pass on most compliance testing. There's plenty more nuance to them of course (keep reading for that), but this is the key distinction. In Traditional 401(k) plans, employer contributions are allowed but not required—and you face the added burden of annual testing. As with all things in life, Safe Harbor plans come with tradeoffs. Matching your employees’ contributions—or contributing regardless of whether they do through what’s called a nonelective contribution—is great for your employees' financial wellbeing, but it could also increase your overall employee budget by 3% or more depending on the size of your contribution. How nondiscrimination testing can trip up small businesses Federal law requires annual nondiscrimination tests, which help ensure 401(k) plans benefit all employees—not just business owners or highly compensated employees (HCEs). Because the federal government provides significant tax perks through 401(k) plans, it wants to make sure these benefits don’t more heavily favor high earners. The three main nondiscrimination tests are: Actual deferral percentage (ADP) test—Compares the average salary deferrals of HCEs to those of non-highly compensated employees (NHCEs). Actual contribution percentage (ACP) test—Compares the average employer matching contributions received by HCEs and NHCEs. Top-heavy test—Evaluates whether a plan is top-heavy, that is, if the total value of the plan accounts of “key employees” is more than 60% of the value of all plan assets. The IRS defines a key employee as an officer making more than $200,000 in 2022 (indexed), an owner of more than 5% of the business, or an owner of more than 1% of the business who made more than $150,000 during the plan year. In practice, it’s easier for large companies to pass the tests because they have a lot of employees at many different income levels contributing to the plan. If, on the other hand, even just a few HCEs at a small-to-midsize business contribute a lot to the plan, but the lower earners don’t, there’s a chance the 401(k) plan will not pass nondiscrimination testing. You may be wondering: “What happens if my plan fails?” Well, you’ll need to fix the imbalance by either returning a portion of the contributions made by your highly compensated employees or by increasing the contributions of your non-highly compensated employees. If you have to refund contributions, affected employees may fall behind on their retirement savings—and that money may be subject to state and federal taxes! If you don’t correct the issue in a timely manner, there could also be a 10% penalty fee and other serious consequences. Failing these tests, in other words, can be a real pain in the pocketbook. Safe Harbor may make sense for you if … Every company is different, but here’s a list of employer characteristics that tend to align best with the plan type. Your staff count is in the dozens, not hundreds. Not all small businesses are created equal. In general, however, the smaller your staff count, the more likely it is that the 401(k) contributions of high earners could outweigh those of their lower-compensated peers. If that happens under a Traditional 401(k) plan, you’re at a higher risk of failing nondiscrimination testing. Your staff includes a high percentage of part-time and/or seasonal employees. For companies with more fluid staff makeups, the same elevated risk of failing nondiscrimination testing applies. These types of workers are typically allowed to participate in plans yet often don’t contribute, thus negatively impacting testing. Your company has previously failed ADP or ACP compliance tests. This one’s a no-brainer. If Traditional 401(k) plans have given you testing fits in recent years, switching to a Safe Harbor plan could help avoid these costly tripups. Your company’s previous plans have been deemed “top-heavy.” Similar to the above, if you haven’t recently failed an ADP or ACP test as part of a Traditional 401(k) plan, but your plan was deemed “top-heavy,” you may have a higher risk of failing in the future. Your company has consistent and adequate cash flow. Safe Harbor 401(k) plans offer employees a pretty sweet deal. The company kicks in a minimum of 3-4% of their salaries, either contingent on a matching contribution or not (see: nonelective). That money vests immediately, too, which means employees can quit tomorrow and keep it. This commitment to your workforce’s retirement savings is the key cost consideration of Safe Harbor plans. It’s why we typically don’t recommend them for companies with less predictable cash flow year-over-year. You’d rather avoid administrative burdens. Take it from us: even successful compliance testing can be a hassle. And failures? They can lead not only to the aforementioned penalties but to uncomfortable conversations with impacted employees. They’ll need explanations for why their contributions are being returned, and they ultimately may not be able to maximize their 401(k). If you prefer peace-of-mind over these compliance worries, consider the Safe Harbor option. Safe Harbor setup deadlines If you’re strongly considering setting up a Safe Harbor plan or adding a Safe Harbor contribution to your existing plan, here are a few key deadlines you need to know: Starting a new plan For calendar year plans, October 1 is the final deadline for starting a new Safe Harbor 401(k) plan. But don’t cut it too close—you’re required to notify your employees 30 days before the plan starts—and you’ll likely need to talk to your plan provider before that. If we’re fortunate enough to serve in that role for you, that means we’ll need to sign a service agreement by August 1. Adding Safe Harbor to an existing plan If you want to add a Safe Harbor match provision to your current plan, you can include a plan amendment that goes into effect January 1 so long as employees receive notice at least 30 days prior. At Betterment, the deadline for you to request this amendment is October 31. Thanks to the SECURE Act, plans that want to become a nonelective Safe Harbor plan—meaning the employer contributes regardless of whether the employee does—have newfound flexibility. An existing plan can implement a 3% nonelective Safe Harbor provision for the current plan year if amended 30 days before the close of the plan year. Plans that decide to implement a nonelective Safe Harbor contribution of 4% or more have until the end of the following year in which the plan will become a Safe Harbor. Communicating with employees Every year, eligible employees need to be notified about their rights and obligations under your Safe Harbor plan (except for those with nonelective contributions, as noted above). The IRS requires notice be given between 30-90 days before the beginning of the plan year. What Betterment at Work brings to your Safe Harbor 401(k) setup An experienced plan provider like Betterment at Work can bring a lot to the table: Smooth onboarding | We guide you through each step of the onboarding process so you can start your plan quickly and easily. Simple administration | Our intuitive tech and helpful team keep you informed of what you need to do, when you need to do it. Affordability | We’re fully transparent about our pricing so no surprises await you or your employees. Investing choice | Give your employees access to a variety of low-cost, expert-built portfolios. Ready to get started – or simply get more of your questions answered? Reach out today. Or keep reading to learn more about whether a Qualified Automatic Contribution Arrangement (QACA) – i.e. auto-enrollment – is right for your Safe Harbor plan. -

![]()

What is a 401(k) QDIA?

A QDIA (Qualified Default Investment Alternative) is the plan’s default investment. When money ...

What is a 401(k) QDIA? A QDIA (Qualified Default Investment Alternative) is the plan’s default investment. When money is contributed to the plan, it’s automatically invested in the QDIA. What is a QDIA? A 401(k) QDIA (Qualified Default Investment Alternative) is the investment used when an employee contributes to the plan without having specified how the money should be invested. As a "safe harbor," a QDIA relieves the employer from liability should the QDIA suffer investment losses. Here’s how it works: When money is contributed to the plan, it’s automatically invested in the QDIA that was selected by the plan fiduciary (typically, the business owner or the plan sponsor). The employee can leave the money in the QDIA or transfer it to another plan investment. When (and why) was the QDIA introduced? The concept of a QDIA was first introduced when the Pension Protection Act of 2006 (PPA) was signed into law. Designed to boost employee retirement savings, the PPA removed barriers that prevented employers from adopting automatic enrollment. At the time, fears about legal liability for market fluctuations and the applicability of state wage withholding laws had prevented many employers from adopting automatic enrollment—or had led them to select low-risk, low-return options as default investments. The PPA eliminated those fears by amending the Employee Retirement Income Security Act (ERISA) to provide a safe harbor for plan fiduciaries who invest participant assets in certain types of default investment alternatives when participants do not give investment direction. To assist employers in selecting QDIAs that met employees’ long-term retirement needs, the Department of Labor (DOL) issued a final regulation detailing the characteristics of these investments. Learn more about what kinds of investments qualify as QDIAs below. Why does having a QDIA matter? When a 401(k) plan has a QDIA that meets the DOL’s rules, then the plan fiduciary is not liable for the QDIA’s investment performance. Without a QDIA, the plan fiduciary is potentially liable for investment losses when participants don’t actively direct their plan investments. Plus, having a QDIA in place means that employee accounts are well positioned—even if an active investment decision is never taken. If you select an appropriate default investment for your plan, you can feel confident knowing that your employees’ retirement dollars are invested in a vehicle that offers the potential for growth. Does my retirement plan need a QDIA? Yes, it’s a smart idea for all plans to have a QDIA. That’s because, at some point, money may be contributed to the plan, and participants may not have an investment election on file. This could happen in a number of situations, including when money is contributed to an account but no active investment elections have been established, such as when an employer makes a contribution but an employee isn’t contributing to the plan; or when an employee rolls money into the 401(k) plan prior to making investment elections. It makes sense then, that plans with automatic enrollment must have a QDIA. Are there any other important QDIA regulations that I need to know about? Yes, the DOL details several conditions plan sponsors must follow in order to obtain safe harbor relief from fiduciary liability for investment outcomes, including: A notice generally must be provided to participants and beneficiaries in advance of their first QDIA investment, and then on an annual basis after that Information about the QDIA must be provided to participants and beneficiaries which must include the following: An explanation of the employee’s rights under the plan to designate how the contributions will be invested; An explanation of how assets will be invested if no action taken regarding investment election; Description of the actual QDIA, which includes the investment objectives, characteristics of risk and return, and any fees and expenses involved Participants and beneficiaries must have the opportunity to direct investments out of a QDIA as frequently as other plan investments, but at least quarterly For more information, consult the DOL fact sheet. What kinds of investments qualify as QDIAs? The DOL regulations don’t identify specific investment products. Instead, they describe mechanisms for investing participant contributions in a way that meets long-term retirement saving needs. Specifically, there are four types of QDIAs: An investment service that allocates contributions among existing plan options to provide an asset mix that takes into account the individual’s age or retirement date (for example, a professionally managed account like the one offered by Betterment) A product with a mix of investments that takes into account the individual’s age or retirement date (for example, a life-cycle or target-date fund) A product with a mix of investments that takes into account the characteristics of the group of employees as a whole, rather than each individual (for example, a balanced fund) The fourth type of QDIA is a capital preservation product, such as a stable value fund, that can only be used for the first 120 days of participation. This may be an option for Eligible Automatic Contribution Arrangement (EACA) plans that allow withdrawals of unintended deferrals within the first 90 days without penalty. We’re excluding further discussion of this option here since plans must still have one of the other QDIAs in cases where the participant takes no action within the first 120 days. What are the pros and cons of each type of QDIA? Let’s breakdown each of the first three QDIAs: 1. An investment service that allocates contributions among existing plan options to provide an asset mix that takes into account the individual’s age or retirement date Such an investment service, or managed account, is often preferred as a QDIA over the other options because they can be much more personalized. This is the QDIA provided as part of Betterment 401(k)s. Betterment factors in more than just age (or years to retirement) when assigning participants their particular stock-to-bond ratio within our Core portfolios. We utilize specific data including salary, balance, state of residence, plan rules, and more. And while managed accounts can be pricey, they don’t have to be. Betterment’s solution, which is relatively lower in cost due to investing in exchange traded funds (ETFs) portfolios, offers personalized advice and an easy-to-use platform that can also take external and spousal/partner accounts into consideration. 2. A product with a mix of investments that takes into account the individual’s age or retirement date When QDIAs were introduced in 2006, target date funds were the preferred default investment. The concept is simple: pick the target date fund with the year that most closely matches the year the investor plans to retire. For example, in 2020 if the investor is 45 and retirement is 20 years away, the 2040 Target Date Fund would be selected. As the investor moves closer to their retirement date, the fund adjusts its asset mix to become more conservative. One common criticism of target date funds today is that the personalization ends there. Target date funds are too simple and their one-size-fits-all portfolio allocations do not serve any individual investor very well. Plus, target date funds are often far more expensive compared to other alternatives. Finally, most target date funds are composed of investments from the same company—and very few fund companies excel at investing across every sector and asset class. Many experts view target date funds as outdated QDIAs and less desirable than managed accounts. 3. A product with a mix of investments that takes into account the characteristics of the group of employees as a whole This kind of product—for example, a balanced fund—offers a mix of equity and fixed-income investments. However, it’s based on group demographics and not on the retirement needs of individual participants. Therefore, using a balanced fund as a QDIA is a blunt instrument that by definition will have an investment mix that is either too heavily weighted to one asset class or another for most participants in your plan. Better QDIAs—and better 401(k) plans Betterment provides tailored allocation advice based on what each individual investor needs. That means greater personalization—and potentially greater investment results—for your employees. At Betterment, we monitor plan participants’ investing progress to make sure they’re on track to reach their goals. When they’re not on target, we provide actionable advice to help get them back on track. As a 3(38) investment manager, we assume full responsibility for selecting and monitoring plan investments—including your QDIA. That means fiduciary relief for you and better results for your employees. The exchange-traded fund (ETF) difference Another key component that sets Betterment apart from the competition is our exclusive use of ETFs. Here's why we use them: Low cost—ETFs generally cost less than mutual funds, which means more money stays invested. Diversified—All of the portfolios used by Betterment are designed with diversification in mind, so that investors are not overly exposed to individual stocks, bonds, sectors, or countries—which may mean better returns in the long run. Efficient—ETFs take advantage of decades of technological advances in buying, selling, and pricing securities. Helping your employees live better Our mission is simple: to empower people to do what’s best for their money so they can live better. Betterment’s suite of financial wellness solutions, from our QDIAs to our user-friendly investment platform, is designed to give your employees a more personalized experience. We invite you to learn more about what we can do for you. -

![]()

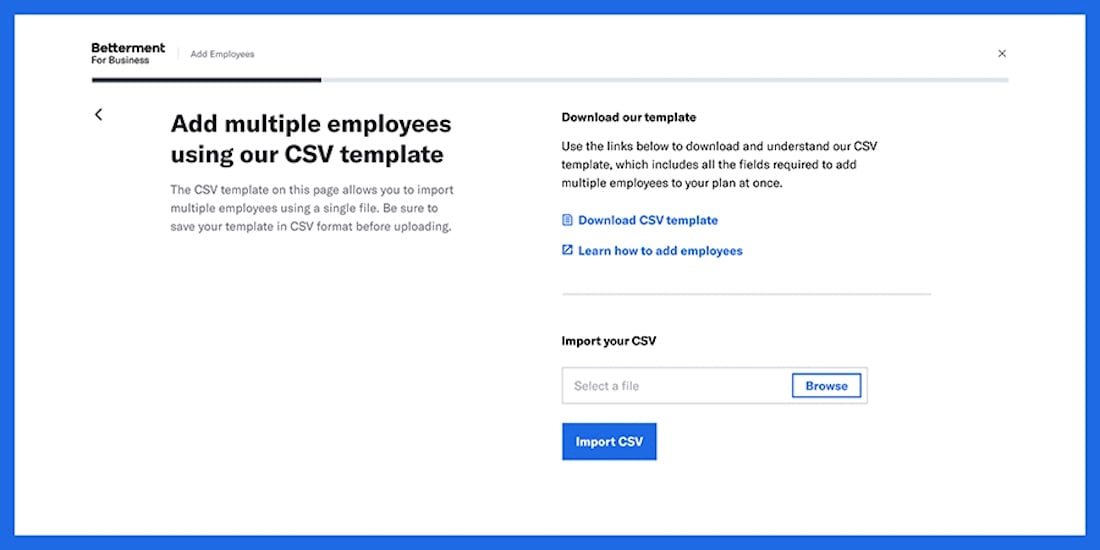

Betterment 401(k) – Bulk Upload Tutorial for Plan Sponsors

Betterment’s bulk upload tool allows you to add multiple employees to your plan quickly. This ...

Betterment 401(k) – Bulk Upload Tutorial for Plan Sponsors Betterment’s bulk upload tool allows you to add multiple employees to your plan quickly. This tutorial outlines best practices and shares helpful tips for using our bulk upload tool effectively. Step-by-step Tutorial Log in to the employer dashboard Navigate to: employees → add employees → add multiple employees Download the CSV template Open the CSV template using a program like Microsoft Excel, Apple Numbers, or Google Sheets Fill out one row for each employee you want to upload. Use the table below to understand the columns in the template: Column Description First Name The employee’s legal first name No special characters accepted Last Name The employee’s legal last name No special characters accepted Middle Initial Leave blank if the employee doesn’t have a legal middle name Social Security Number The employee’s government-issued Social Security Number If the employee is not a US Citizen, a Social Security Number still needs to be provided Social Security Numbers should be formatted with hyphens, e.g.: 123-45-6789 Email Betterment uses email to complete the employee sign-up process and to send employees important plan notifications and updates Date of Birth Date should be formatted as MM/DD/YYYY Employment Status This field accepts the following inputs: active (currently employed) terminated (formerly employed) deceased (deceased) disabled (on disability leave) unpaid_leave (unpaid leave) retired (retired former employee) Date of Hire Date of hire can be up to one year in the future Date should be formatted as MM/DD/YYYY Date of Termination This field is required if Employment Status is terminated, deceased, disabled or retired This field can be left blank for employees who are active or who are on unpaid leave Date of termination can be up to one year in the future Date should be formatted as MM/DD/YYYY Date of Rehire This field is required if Employment Status is active and Date of Termination is set Address Line 1 This field is required for all employees The employee’s residential address cannot be a PO Box If the employee’s address includes a comma, you must put that address within quotation marks Address Line 2 This field can be left blank if the employee’s residential address is only one line City Part of the employee’s residential address State Part of the employee’s residential address State should be written using the official two-letter postal abbreviation Examples: NY, FL, CA, TX 5 Digit ZIP Code Part of the employee’s residential address Eligible This field accepts an input of Y or N If an employee will be hired in the future, you must enter N for Eligible, and enter a date in the Entry on column. This indicates that the employee will become eligible for the plan on the future date you’ve specified. Entry on This field defines the date on which an employee will become eligible for the 401(k) plan This date can be in the past or the future Date should be formatted as MM/DD/YYYY Electronic Access This field accepts an input of Y or N Can this employee receive emails and access Betterment’s website at a computer they use regularly as part of their job? Union Member This field accepts an input of Y or N Is this employee a member of a union? Date Joined Union Required if the employee is a member of a union Date should be formatted as MM/DD/YYYY Can be left blank for non-union employees Participant Type This field accepts the following inputs: primary (all participants who are currently in the plan, whether active, terminated, deceased, disabled, retired, or on leave) beneficiary (beneficiary of a deceased participant) alternate_payee (a person who will be the payee of a divorce or other legal settlement) Deferral Rate If an employee was participating in a 401(k) plan you had with a previous provider, please indicate their contribution rate from that provider. This will be used as their new default rate at Betterment. The employee will be able to log into their account to change this prior to their first contribution with Betterment. Traditional deferral amount and percent cannot both be present. Roth deferral amount and percent cannot both be present. If you’re not switching to Betterment from a previous provider, you can leave this field blank. After you’re done filling out the document, export the file as a CSV. Upload your CSV file to Betterment. If you receive any errors after uploading your file, review the errors and make changes to your CSV file. Re-upload the file to Betterment after making changes. Once your file is accepted without any errors, you’ll be asked to review the names of the newly created employees. This helps ensure that you’re uploading the correct file to your plan. When you’re done reviewing, click the ‘add employees’ button. Next, the upload process will begin. Once your employees have been uploaded, they’ll receive an email inviting them to complete the sign-up process. Finally, check the employees page to make sure there are no outstanding errors that occurred during the employee creation process. Address any errors that may have occurred. You’re all set! All new participant profiles will be visible on the employees page. You can return to the employees page to make changes to an employee’s profile at any time. Frequently Asked Questions Do I have to do anything else? Nope! You’re all set. Betterment will email all required disclosures to your new plan participants. Do I have to send any notices to my employees? No, Betterment will send all notices to your employees automatically via email. When will my employees be alerted? Employees will be notified by email as soon as their account is created. How can my employees join the plan after I upload their information to Betterment? Employees can check their email for an invite from Betterment to complete the sign-up process. My employee has a P.O. Box as their address. Can I use that address with Betterment? No. To comply with regulations for opening accounts, we require a physical address to verify an employee's identity. Betterment will not send physical mail to an employee’s address (unless they opt into paper statements, which is rare); we will otherwise only use their physical address for account verification. Questions? Contact us.

All 401K Plan Setup articles

-

![]()

Plan Design Matters

Plan Design Matters Thoughtful 401(k) plan design can help motivate even reluctant retirement savers to start investing for their future. Designing a 401(k) plan is like building a house. It takes care, attention, and the help of a few skilled professionals to create a plan that works for both you and your employees. In fact, thoughtful plan design can help motivate even reluctant retirement savers to start investing for their future - read more to learn how. How to tailor a 401(k) plan you and your employees will love As you embark on the 401(k) design process, there are many options to consider. In this article, we’ll take you through the most important choices so you can make well-informed decisions. Since certain choices may not be available on the various pricing models of any given provider, make sure you understand your options and the trade-offs you’re making. Let’s get started! 401(k) eligibility When would you like employees to be eligible to participate in the plan? You can opt to have employees become eligible: Immediately – as soon as they begin working for your company After a specific length of service – for example, a period of hours, months, or years of service It’s also customary to have an age requirement (for example, employees must be 18 years or older to participate in the plan). You may also want to consider an “employee class exclusion” to prevent part-time, seasonal, or temporary employees from participating in the plan. Once employees become eligible, they can immediately enroll – or, you can restrict enrollment to a monthly, quarterly, or semi-annual basis. If you have immediate 401(k) eligibility and enrollment, in theory, more employees could participate in the plan. However, if your company has a higher rate of turnover, you may want to consider adding service length requirements to alleviate the unnecessary administrative burden of having to maintain many small accounts of employees who are no longer with your organization. Enrollment Enrollment is another important feature to consider as you structure your plan. You may simply allow employees to enroll on their own, or you can add an automatic enrollment feature. Automatic enrollment (otherwise known as auto-enrollment) allows employers to automatically deduct elective deferrals from employees’ wages unless they elect not to contribute. With automatic enrollment, all employees are enrolled in the plan at a specific contribution rate when they become eligible to participate in the plan. Employees have the freedom to opt out and change their contribution rate and investments at any time. As you can imagine, automatic enrollment can have a significant impact on plan participation. In fact, according to research by The Defined Contribution Institutional Investment Association (DCIIA), automatic enrollment 401(k) plans have participation rates greater than 90%! That’s in stark contrast to the roughly 50% participation rate for plans in which employees must actively opt in. If you decide to elect automatic enrollment, consider your default contribution rate carefully. A 3% default contribution rate is still the most popular; however, more employers are electing higher default rates because research shows that opt-out rates don’t appreciably change even if the default rate is increased. Many financial experts recommend a retirement savings rate of 10% to 15%, so using a higher automatic enrollment default rate would give employees even more of a head start. Auto-escalation Auto-escalation is an important feature to look out for as you design your plan. It enables employees to increase their contribution rate over time as a way to increase their savings. With auto-escalation, eligible employees will automatically have their contribution rate increased by 1% every year until they reach a maximum cap of 15%. Employees can also choose to set their own contribution rate at any time, at which point they will no longer be enrolled in the auto-escalation feature. For example, if an employee is auto-enrolled at 6% with a 1% auto-escalation rate, and they choose to change their contribution rate to 8%, they will no longer be subject to the 1% increase every year. Compensation You’re permitted to exclude certain types of compensation for plan purposes, including compensation earned prior to plan entry and fringe benefits for purposes of compliance testing and allocating employer contributions. You may choose to define your compensation as: W2 (box 1 wages) plus deferrals – Total taxable wages, tips, prizes, and other compensation 3401(a) wages – All wages taken into account for federal tax withholding purposes, plus the required additions to W-2 wages listed above Section 415 Safe Harbor – All compensation received from the employer which is includible in gross income Employer contributions Want to encourage employees to enroll in the plan? Free money is a great place to start! That’s why more employers are offering profit sharing or matching contributions. Some common employer contributions are: Safe harbor contributions – With the added bonus of being able to avoid certain time-consuming compliance tests, safe harbor contributions often follow one of these formulas: Basic safe harbor match—Employer matches 100% of employee contributions, up to 3% of their compensation, plus 50% of the next 2% of their compensation. Enhanced safe harbor match—The most common employer match formula is 100% of employee contributions, up to 4% of their compensation, but this could vary. Non-elective contribution—Employer contributes at least 3% of each employee’s compensation, regardless of whether they make their own contributions. Discretionary matching contributions – You decide what percentage of employee 401(k) deferrals to match and the maximum percentage of pay to match. For example, you could elect to match 50% of contributions on up to 6% of compensation. One advantage of having a discretionary matching contribution is that you retain the flexibility to adjust the matching rate as your business needs change. Non-elective contributions – Each pay period, you have the option of contributing to your employees’ 401(k) accounts, regardless of whether they contribute. For example, you could make a profit sharing contribution (one type of non-elective contribution) at the end of the year as a percentage of employees’ salaries or as a lump-sum amount. In addition to helping your employees build their retirement nest eggs, employer contributions are also tax deductible (up to 25% of total eligible compensation), so it may cost less than you think. Plus, we believe offering an employer contribution can play a key role in recruiting and retaining top employees. 401(k) vesting If you elect to make an employer contribution, you also need to decide on a vesting schedule (an employee’s own contributions are always 100% vested). Note that all employer contributions made as part of a safe harbor plan are immediately and 100% vested (although QACA plans can be subject to a 2-year cliff). The three main vesting schedules are: Immediate – Employees are immediately vested in (or own) 100% of employer contributions as soon as they receive them. Graded – Vesting takes place in a gradual manner. For example, a six-year graded schedule could have employees vest at a rate of 20% a year until they are fully vested. Cliff – The entire employer contribution becomes 100% vested all at once, after a specific period of time. For example, if you had a three-year cliff vesting schedule and an employee left after two years, they would not be able to take any of the employer contributions (only their own). Like your eligibility and enrollment decisions, vesting can also have an impact on employee participation. Immediate vesting may give employees an added incentive to participate in the plan. On the other hand, a longer vesting schedule could encourage employees to remain at your company for a longer time. Service counting method If you decide to use length of service to determine your eligibility and vesting schedules, you must also decide how to measure it. Typically, you may use: Elapsed time – Period of service as long as employee is employed at the end of period Actual hours – Actual hours worked. With this method, you’ll need to track and report employee hours Actual hours/equivalency – A formula that credits employees with set number of hours per pay period (for example, monthly = 190 hours) 401(k) withdrawals and loans Naturally, there will be times when your employees need to withdraw money from their retirement accounts. Your plan design will have rules outlining the withdrawal parameters for: Termination In-service withdrawals (at attainment of age 59 ½; rollovers at any time) Hardships Qualified Domestic Relations Orders (QDROs) Required Minimum Distributions (RMDs) Plus, you’ll have to decide whether to allow participants to take 401(k) plan loans (and the maximum amount of the loan). While loans have the potential to derail employees’ retirement dreams, having a loan provision means employees can access their money if they need it and employees can pay themselves back plus interest. If employees are reluctant to participate because they’re afraid their savings will be “locked up,” then a loan provision can help alleviate that fear. Investment options When it comes to investment methodology, there are many strategies to consider. Your plan provider can help guide you through the choices and associated fees. For example, at Betterment, we believe that our expert-built ETF portfolios offer investors significant diversification and flexibility at a low cost. Plus, we offer ETFs in conjunction with personalized advice to help today’s retirement savers pursue their goals. Get help from the experts Your 401(k) plan provider can walk you through your plan design choices and help you tailor a plan that works for your company and your employees. Once you’ve settled on your plan design, you will need to codify those features in the form of a formal plan document to govern your 401(k) plan. At Betterment, we draft the plan document for you and provide it to you for review and final approval. Your business is likely to evolve—and your plan design can evolve, too. Drastic increase in profits? Consider adding an employer match or profit sharing contribution to share the wealth. Plan participation stagnating? Consider adding an automatic enrollment feature to get more employees involved. Employees concerned about access to their money in an uncertain world? Consider adding a 401(k) loan feature. Need a little help figuring out your plan design? Talk to Betterment. Our experts make it easy for you to offer your employees a better 401(k) —at one of the lowest costs in the industry. -

![]()

Understanding 401(k) Fees

Understanding 401(k) Fees Come retirement time, the number of 401(k) plan fees charged can make a major difference in your employees’ account balances—and their futures. Did you know that the smallest 401(k) plans often pay the most in fees? We believe that you don’t have to pay high fees to provide your employees with a top-notch 401(k) plan. In fact, Betterment offers comprehensive plan solutions at one of the lowest costs in the industry. Why do 401(k) fees matter? The difference between a 1% fee and a 2% fee may not sound like much, but in reality, higher 401(k) fees can take a major bite out of your participants’ retirement savings. Consider this example: Triplets Jane, Julie, and Janet each began investing in their employers’ 401(k) plan at the age of 25. Each had a starting salary of $50,000, increased by 3% annually, and contributed 6% of their pre-tax salary with no company matching contribution. Their investments returned 6% annually. The only difference is that their retirement accounts were charged annual 401(k) fees of 1%, 1.5%, and 2%, respectively. Forty years later, they’re all thinking about retiring and decide to compare their account balances. Here’s what they look like: Annual 401(k) fee Account balance at age 65 Jane 1% $577,697 Julie 1.5% $517,856 Janet 2% $465,894 Information is hypothetical and provided for educational purposes only. As such, these figures do not reflect Betterment’s management fee and do not reflect any actual client performance As you can see, come retirement time, the amount of fees charged can make a major difference in your employees’ account balances—and their futures. Why should employers care about 401(k) fees? You care about your employees, so naturally, you want to help them build brighter futures. But beyond that, it’s your fiduciary duty as a plan sponsor to make sure you’re only paying reasonable 401(k) fees for services that are necessary for your plan. The Department of Labor (DOL) outlines rules that you must follow to fulfill this fiduciary responsibility, including “ensuring that the services provided to the plan are necessary and that the cost of those services is reasonable” and has published a guide to assist you in this process. Generally, any firm providing services of $1,000 or more to your 401(k) plan is required to provide a fee disclosure, which is the first step in understanding your plan’s fees and expenses. It’s important to note that the regulations do not require you to ensure your fees are the lowest available, but that they are reasonable given the level and quality of service and support you and your employees receive. Benchmark the fees against similar retirement plans (by number of employees and plan assets, for example) to see if they’re reasonable. What are the main types of fees? Typically, 401(k) fees fall into three categories: administrative fees, individual service fees, and investment fees. Let’s dig a little deeper into each category: Plan administration fees—Paid to your 401(k) provider, plan administration fees typically cover 401(k) set-up fees, as well as general expenses such as recordkeeping, communications, support, legal, and trustee services. These costs are often assessed as a flat annual fee. Investment fees—Investment fees, typically assessed as a percentage of assets under management, may take two forms: fund fees that are expressed as an expense ratio or percentage of assets, and investment advisory fees for portfolio construction and the ongoing management of the plan assets. Betterment, for instance, acts as investment advisor to its 401(k) clients, assuming full fiduciary responsibility for the selection and monitoring of funds. And as is also the case with Betterment, the investment advisory fee may even include personalized investment advice for every employee. Individual service fees—If participants elect certain services—such as taking out a 401(k) loan—they may be assessed individual fees for each service. Wondering what you and your employees are paying in 401(k) fees? Fund fees are detailed in the funds’ prospectuses and are often wrapped up into one figure known as the expense ratio, expressed as a percentage of assets. Other fees are described in agreements with your service providers. High quality, low fees Typically, mutual funds have dominated the retirement investment landscape, but in recent years, exchange-traded funds (ETFs) have become increasingly popular. At Betterment, we believe that a portfolio of ETFs, in conjunction with personalized, unbiased advice, is the ideal solution for today’s retirement savers. Who pays 401(k) fees: the employer or the participant? The short answer is that it depends. As the employer, you may have options with respect to whether certain fees may be allocated to plan participants. Expenses incurred as a result of plan-related business expenses (so-called “ settlor expenses”) cannot be paid from plan assets. An example of such an expense would be a consulting fee related to the decision to offer a plan in the first place. Other costs associated with plan administration are eligible to be charged to plan assets. Of course, just because certain expenses can be paid by plan assets doesn’t mean you are off the hook in monitoring them and ensuring they remain reasonable. Plan administration fees are often paid by the employer. While it could be a significant financial responsibility for you as the business owner, there are three significant upsides: Reduced fiduciary liability—As you read, paying excessive fees is a major source of fiduciary liability. If you pay for the fees from a corporate account, you reduce potential liability. Lowered income taxes—If your company pays for the administration fees, they’re tax deductible! Plus, you can potentially save even more with the new SECURE Act tax credits for starting a new plan and for adding automatic enrollment. Increased 401(k) returns—Do you take part in your own 401(k) plan? If so, paying 401(k) fees from company assets means you’ll be keeping more of your personal retirement savings. Fund fees are tied to the individual investment options in each participant’s portfolio. Therefore, these fees are paid from each participant’s plan assets. Individual service fees are also paid directly by investors who elect the service, for example, taking a plan loan. How can you minimize your 401(k) fees? Minimizing your fees starts with the 401(k) provider you choose. In the past, the price for 401(k) plan administration was quite high. However, things have changed, and now the era of expensive, impersonal, unguided retirement saving is over. Innovative companies like Betterment now offer comprehensive plan solutions at a fraction of the cost of most providers. Betterment combines the power of efficient technology with personalized advice so that employers can provide a benefit that’s truly a benefit, and employees can know that they’re invested correctly for retirement. No hidden fees. Maximum transparency. Costs are often passed to the employee through fund fees, and in fact, mutual fund pricing structures incorporate non-investment fees that can be used to pay for other types of expenses. Because they are embedded in mutual fund expense ratios, they may not be explicit, therefore making it difficult for you to know exactly how much you and your employees are paying. In other words, most mutual funds in 401(k) plans contain hidden fees. At Betterment, we believe in transparency. Our use of ETFs means there are no hidden fees, so you and your employees are able to know how much you’re paying for the underlying investments themselves. Plus, our pricing structure unbundles the key offerings we provide—advisory, investment, record keeping, and compliance—and assigns a fee to each service. A clearly defined fee structure means no surprises for you—and more money working harder for your employees. -

![]()

401(k) Glossary of Terms

401(k) Glossary of Terms Whether you're offering a 401(k) for the first time or need a refresh on important terms, these definitions can help you make sense of industry jargon. 3(16) fiduciary: A fiduciary partner hired by an employer to handle a plan’s day-to-day administrative responsibilities and ensure that the plan remains in compliance with Department of Labor regulations. 3(21) fiduciary: An investment advisor who acts as co-fiduciary to review and make recommendations regarding a plan’s investment lineup. This fiduciary provides guidance but does not have the authority to make investment decisions. 3(38) fiduciary: A codified retirement plan fiduciary that’s responsible for choosing, managing, and overseeing the plan’s investment options. 401(k) administration costs: The expenses involved with the various aspects of running a 401(k) plan. Plan administration includes managing eligibility and enrollment, coordinating contributions, processing distributions and loans, preparing and delivering legally required notices and forms, and more. 401(k) committee charter: A document that describes the 401(k) committee’s responsibilities and authority. 401(k) compensation limit: The maximum amount of compensation that’s eligible to draw on for plan contributions, as determined by the IRS. In 2020, this limit is $285,000. Keep in mind that contributions are also limited by the 401(k) contribution limit, which is $19,500 in 2020 for those under age 50. 401(k) contribution limits: The maximum amount that a participant may contribute to an employer-sponsored 401(k) plan, as determined by the IRS. For 2020, the limits are $19,500 for individuals under age 50, and $26,000 for individuals age 50 and older (including $6,500 in catch-up contributions). 401(k) force-out rule: Refers to a plan sponsor’s option to remove a former employee’s assets from the retirement plan. The sponsor has the option to “force out” these assets (into an IRA in the former employee’s name) if the assets are less than $5,000. 401(k) plan: An employer-sponsored retirement savings plan that allows participants to save money on a tax-advantaged basis. 401(k) plan fees: The various fees associated with a plan. These can include fees for investment management, plan administration, fiduciary services, and consulting fees. While some fees are applied at the plan level — that is, deducted from plan assets — others are charged directly to participant accounts. 401(k) plan fee benchmarking: The process of comparing a plan’s fees to those of other plans in similar industries with roughly equal assets and participation rates. This practice can help to determine if a plan’s fees are reasonable per ERISA requirements. 401(k) set-up costs: The expenses involved in establishing a 401(k) plan. These costs cover plan documents, recordkeeping, investment management, participant communication, and other essential aspects of the plan. 401(k) withdrawal: A distribution from a plan account. Because a 401(k) plan is designed to provide income during retirement, a participant generally may not make a withdrawal until age 59 ½ unless he or she terminates or retires; becomes disabled; or qualifies for a hardship withdrawal per IRS rules. Any other withdrawals before age 59 ½ are subject to a 10% penalty as well as regular income tax. 404(a)(5) fee disclosure: A notice issued by a plan sponsor that details information about investment fees. This notice, which is required of all plan sponsors by the Department of Labor, covers initial disclosure for new participants, new fees, and fee changes. 404(c) compliance: Refers to a participant’s (or beneficiary’s) right to choose the specific investments for 401(k) plan assets. Because the participant controls investment decisions, the plan fiduciary is not liable for investment losses. 408(b)(2) fee disclosure: A notice issued by a plan service provider that details the fees charged by the provider (and its affiliates or subcontractors) and reports any possible conflicts of interest. The Department of Labor requires all plan fiduciaries to issue this disclosure. Actual contribution percentage (ACP) test: A required compliance test that compares company matching contributions among highly compensated employees (HCEs) and non-highly compensated employees (NHCEs). Actual deferral percentage (ADP) test: A required compliance test that compares employee deferrals among highly compensated employees (HCEs) and non-highly compensated employees (NHCEs). Annual fee disclosure: A notice issued by a plan sponsor that details the plan’s fees and investments. This disclosure includes plan and individual fees that may be deducted from participant accounts, as well as information about the plan’s investments (performance, expenses, fees, and any applicable trade restrictions). Automated Clearing House (ACH): A banking network used to transfer funds between banks quickly and cost-efficiently. Automatic enrollment (ACA): An option that allows employers to automatically deduct elective deferrals into the plan from an employee’s wages unless the employee actively elects not to contribute or to contribute a different amount. Beneficiary: The person or persons who a participant chooses to receive the assets in a plan account if he or she dies. If the participant is married, the spouse is automatically the beneficiary unless the participant designates a different beneficiary (and signs a written waiver). If the participant is not married, the account will be paid to his or her estate if no beneficiary is on file. Blackout notice: An advance notice of an upcoming blackout period. ERISA rules require plan sponsors to notify participants of a blackout period at least 30 days in advance. Blackout period: A temporary period (three or more business days) during which a 401(k) plan is suspended, usually to accommodate a change in plan administrators. During this period, participants may not change investment options, make contributions or withdrawals, or request loans. Catch-up contributions: Contributions beyond the ordinary contribution limit, which are permitted to help people age 50 and older save more as they approach retirement. In 2022, contribution limits (set by the IRS) are $20,500 on ordinary contributions and $6,500 on catch-up contributions, for a combined limit of $27,000. Compensation: The amount of pay a participant receives from an employer. For purposes of 401(k) contribution calculations, only compensation is considered to be eligible. The plan document defines which form, for example the W-2, is referred to in determining the compensation amount. Constructive receipt: A payroll term that refers to the impending receipt of a paycheck. The paycheck has not yet been fully cleared for deposit in the employee’s bank account, but the employee has access to the funds. Deferrals: Another term for contributions made to a 401(k) account. Defined contribution plan: A tax-deferred retirement plan in which an employee or employer (or both) invest a fixed amount or percentage (of pay) in an account in the employee’s name. Participation in this type of plan is voluntary for the employee. A 401(k) plan is one type of tax-deferred defined contribution plan. Department of Labor (DOL): The federal government department that oversees employer-sponsored retirement plans as well as work-related issues including wages, hours worked, workplace safety, and unemployment and reemployment services. Distributions: A blanket term for any withdrawal from a 401(k) account. A distribution can include a required minimum distribution (RMD), a loan, a hardship withdrawal, a residential loan, or a qualified domestic relations order (QDRO). Docusign: A third-party platform used for exchanging signatures on documents, especially during plan onboarding. EIN: An Employer Identification Number (EIN) is also known as a Federal Tax Identification Number, and is used to identify a business entity. Eligible automatic enrollment arrangement (EACA): An automatic enrollment (ACA) plan that applies a default and uniform deferral percentage to all employees who do not opt out of the plan or provide any specific instructions about deferrals to the plan. Under this arrangement, the employer is required to provide employees with adequate notice about the plan and their rights regarding contributions and withdrawals. ERISA: Refers to the Employee Retirement Income Security Act of 1974, a federal law that requires individuals and entities that manage a retirement plan (fiduciaries) to follow strict standards of conduct. ERISA rules are designed to protect retirement plan participants and secure their access to benefits in the plan. Excess contributions: The amount of contributions to a plan that exceed the IRS contribution limit. Excess contributions made in any year (and their earnings) may be withdrawn without penalty by the tax filing deadline for that year, and the participant is then required to pay regular taxes on the amount withdrawn. Any excess contributions not withdrawn by the tax deadline are subject to a 6% excise tax every year they remain in the account. Exchange-traded fund (ETF): Passively managed index funds that feature low costs and high liquidity. ETFs make it easy to manage portfolios efficiently and effectively. All of Betterment’s 401(k) investment options are ETFs. Fee disclosure: Information about the various fees related to a 401(k) plan, including plan administration, fiduciary services, and investment management. Fee disclosure deadline: The date by which a plan sponsor must provide plan and investment-related fee disclosure information to participants. The DOL requires you to send your participant fee disclosure notice at least once in any 14-month period without regard to whether the plan operates on a calendar-year or fiscal-year basis. Fidelity bond: Also known as a fiduciary bond, this bond protects the plan from losses due to fraud or dishonesty. Every fiduciary who handles 401(k) plan funds is required to hold a fidelity bond. Fiduciary: An individual or entity that manages a retirement plan and is required to always act in the best interests of employees who save in the plan. In exchange for helping employees build retirement savings, employers and employees receive special tax benefits, as outlined in the Internal Revenue Code. When a company adopts a 401(k) plan for employees, it becomes an ERISA fiduciary and takes on two sets of fiduciary responsibilities: “Named fiduciary” with overall responsibility for the plan, including selecting and monitoring plan investments “Plan administrator” with fiduciary authority and discretion over how the plan is operated Most companies hire one or more outside experts (such as an investment advisor, investment manager, or third-party administrator) to help manage their fiduciary responsibilities. Form 5500: An informational document that a plan sponsor must prepare to disclose the identity of the plan sponsor (including EIN and plan number), characteristics of the plan (including auto-enrollment, matching contributions, profit-sharing, and other information), the numbers of eligible and active employees, plan assets, and fees. The plan sponsor must submit this form annually to the IRS and the Department of Labor, and must provide a summary to plan participants. Smaller plans (less than 100 employees) may instead file Form 5500-SF. Hardship withdrawal: A withdrawal before age 59 ½ intended to address a severe and immediate need (as defined by the IRS). To qualify for a hardship withdrawal, a participant must provide the employer with documentation (such as a medical bill, a rent invoice, funeral expenses) that shows the purpose and amount needed. If the hardship withdrawal is authorized, it must be limited to the amount needed (adjusted for taxes and penalties), may still be subject to early withdrawal penalties, is not eligible for rollover, and may not be repaid to the plan. Highly compensated employee (HCE): An employee who earned at least $125,000 in compensation from the plan sponsor during the previous year (if 2019), or at least $130,000 if the previous year is 2020, or owned more than 5% interest in the plan sponsor’s business at any time during the current or previous year (regardless of compensation). Inception to date (ITD): Refers to contribution amounts since the inception of a participant’s account. Internal Revenue Service (IRS): The U.S. federal agency that’s responsible for the collection of taxes and enforcement of tax laws. Most of the work of the IRS involves income taxes, both corporate and individual. Investment advice (ERISA ruling): The Department of Labor’s final ruling (revised in 2020) on what constitutes investment advice and what activities define the role of a fiduciary. Investment policy statement (IPS): A plan’s unique governing document, which details the characteristics of the plan and assists the plan sponsor in complying with ERISA requirements. The IPS should be written carefully, reviewed regularly, updated as needed, and adhered to closely. Key employee: An employee classification used in top-heavy testing. This is an employee who meets one of the following criteria: Ownership stake greater than 5% Ownership stake greater than 1% and annual compensation greater than $150,000 Officer with annual compensation greater than $200,000 (for 2022) Non-discrimination testing: Tests required by the IRS to ensure that a plan does not favor highly compensated employees (HCEs) over non-highly compensated employees (NHCEs). Non-elective contribution: An employer contribution to an employee’s plan account that’s made regardless of whether the employee makes a contribution. This type of contribution is not deducted from the employee’s paycheck. Non-highly compensated employee (NHCE): An employee who does not meet any of the criteria of a highly compensated employee (HCE). Plan sponsor: An organization that establishes and offers a 401(k) plan for its employees or members. Qualified default investment alternative (QDIA): The default investment for plan participants who don’t make an active investment selection. All 401(k) plans are required to have a QDIA. For Betterment’s 401(k), the QDIA is the Core Portfolio Strategy, and a customized risk level is set for each participant based on their age. Qualified domestic relations order (QDRO): A document that recognizes a spouse’s, former spouse’s, child’s, or dependent’s right to receive benefits from a participant’s retirement plan. Typically approved by a court judge, this document states how an account must be split or reassigned. Plan administrator: An individual or company responsible for the day-to-day responsibilities of 401(k) plan administration. Among the responsibilities of a plan administrator are compliance testing, maintenance of the plan document, and preparation of the Form 5500. Many of these responsibilities may be handled by the plan provider or a third-party administrator (TPA). Plan document: A document that describes a plan’s features and procedures. Specifically, this document identifies the type of plan, how it operates, and how it addresses the company’s unique needs and goals. Professional employer organization (PEO): A firm that provides small to medium-sized businesses with benefits-related and compliance-related services. Profit sharing: A type of defined contribution plan in which a plan sponsor contributes a portion of the company’s quarterly or annual profit to employee retirement accounts. This type of plan is often combined with an employer-sponsored retirement plan. Promissory note: A legal document that lays out the terms of a 401(k) loan or other financial obligation. Qualified non-elective contribution (QNEC): A contribution that a plan is required to make if it’s found to be top-heavy. Required minimum distribution (RMD): Refers to the requirement that an owner of a tax-deferred account begin making plan withdrawals each year starting at age 72. The first withdrawal must be made by April 1 of the year after the participant reaches age 72, and all subsequent annual withdrawals must be made by December 31. Rollover: A retirement account balance that is transferred directly from a previous employer’s qualified plan to the participant’s current plan. Consolidating accounts in this way can make it easier for a participant to manage and track retirement investments, and may also reduce retirement account fees. Roth 401(k) contributions: After-tax plan contributions that do not reduce taxable income. Contributions and their earnings are not taxed upon withdrawal as long as the participant is at least age 59½ and has owned the Roth 401(k) account for at least five years. For 2020, the limits on plan contributions (Traditional, Roth, or a combination of both) are $19,500 for individuals under age 50, and $26,000 for individuals age 50 and older (including $6,500 in catch-up contributions). Roth vs. pre-tax contributions: Pre-tax contributions reduce a participant’s current income, with taxes due when funds are withdrawn (typically in retirement). Alternatively, Roth contributions are deposited into the plan after taxes are deducted, so withdrawals are tax-free. Safe Harbor: A plan design option that provides annual testing exemptions. In exchange, employer contributions on behalf of all employees are required. Saver’s credit: A credit designed to help low- and moderate-income taxpayers further reduce their taxes by saving for retirement. The amount of this credit — 10%, 20%, or 50% of contributions, based on filing status and adjusted gross income — directly reduces the amount of tax owed. Stock option: The opportunity for an employee to purchase shares of an employer’s stock at a specific (often discounted) price for a limited time period. Some companies may offer a stock option as an alternative or a complement to a 401(k) plan. Summary Annual Report (SAR): A summary version of Form 5500, which a plan sponsor is required to provide to participants every year within two months after the Form 5500 deadline – September 30 or December 15 (if there was an extension given for Form 5500 filing). Summary Plan Description (SPD): A comprehensive document that describes in detail how a 401(k) plan works and the benefits it provides. Employers are required to provide an SPD to employees free of charge. Third-party administrator (TPA): An individual or company that may be hired by a 401(k) plan sponsor to help run many day-to-day aspects of a retirement plan. Among the responsibilities of a TPA are compliance testing, generation and maintenance of the plan document, and preparation of Form 5500. Traditional contributions: Pre-tax plan contributions that reduce taxable income. These contributions and their earnings are taxable upon withdrawal, which is typically during retirement. Vesting: Another word for ownership. Participants are always fully vested in the contributions they make. Employer contributions, however, may be subject to a vesting schedule in which participant ownership builds gradually over several years. -

![]()

Is Auto-Enroll Right for Your 401(k) Plan?

Is Auto-Enroll Right for Your 401(k) Plan? Learn the ins and outs of this popular plan feature that streamlines the participant experience. “Maybe when I make more.” “Maybe when I pay off my student loans.” “Maybe when my horoscope tells me it’s time.” When it comes to employees enrolling in their 401(k)s, there’s always a reason why now isn’t the right time. But the fact is the best time to save for retirement is right now, while time and the power of compounding growth are on their side. That’s where 401(k) automatic enrollment—or ‘auto-enroll’ for short—comes in. It gives your employees the gentle nudge they might need to start saving for retirement. Before we dive into auto-enroll and whether it makes sense for your company, let’s take a moment to celebrate your journey toward finding the 401(k) plan that’s right for you! If you’re reading this article, you’ve reached one of the final key considerations of plan design. Another key consideration? That’s whether getting a pass on most compliance testing is worth the employer contribution requirements of a Safe Harbor 401(k) plan. If you go the Safe Harbor route, then your specific flavor of auto-enroll may be called a Qualified Automatic Contribution Arrangement (QACA). We’ll cover QACAs and the two other types of auto-enroll below. How 401(k) auto-enroll works As the name implies, automatic enrollment lets employers automatically deduct elective deferrals from employees’ wages. Simply put, it means your employees don’t have to lift a finger to start saving for retirement. Compare that to the typical enrollment process where employees must go online, make a phone call, or submit paperwork to access their retirement plan. All those little steps take real effort, and employees who are on the fence about enrolling might not be bothered to do it. Before they know it, years have passed, and they’ve missed out on valuable time in the market that they will never get back. Or you can do them a solid and make it all automatic. If you decide to add an automatic enrollment feature to your 401(k) plan, you must notify your employees at least 30 days in advance. After you do, they have three options: Opt out. Employees can opt out of 401(k) plan participation in advance. At Betterment at Work, by the way, we make it simple for employees to do this online. Customize their contribution amount or investments. Instead of enrolling with the default automatic enrollment elections, employees can stay enrolled but choose their own contribution rate. Do nothing for now and enjoy the ride. Here we see the beauty of automatic enrollment. Employees don’t have to do anything to start investing. Once the opt-out timeframe has elapsed, they’ll automatically begin deferring a certain percentage of their pay to their 401(k). Employees are typically informed each year that they can opt out from this enrollment. As you can imagine, option C is a popular choice. Among our clients who use auto-enroll, the employee participation rate is nearly 90 percent. The three types of automatic enrollment Before we go into each, a warning: we’re about to throw even more acronyms at you. If you’re allergic to alphabet soup, prepare accordingly! All three types of auto-enroll require that employees be enrolled at preset contribution rates and have the options to opt out or change their contribution rates. That’s effectively where a Basic Automatic Contribution Arrangement (ACA) begins and ends. Two other varieties add a few more wrinkles on top of that. With an Eligible Automatic Contribution Arrangement (EACA), employees can also request a refund of deferrals within the first 90 days. Employers come to a Qualified Automatic Contribution Arrangement (QACA) by way of a Safe Harbor 401(k) plan. That means they’ve already committed to, among other things, a specific threshold of employer contributions. Safe Harbor plans that include auto-enroll must also steadily increase their employees’ contribution rates each year in what’s often referred to as automatic escalation. We offer auto-escalation at no added expense for all new plans. Here’s how all this shakes out in grid form: Basic Automatic Contribution Arrangement (ACA) Eligible Automatic Contribution Arrangement (EACA) Qualified Automatic Contribution Arrangement (QACA) Employees enrolled at preset contribution rates ✓ ✓ ✓ Employees can opt-out or change contribution rates ✓ ✓ ✓ Employees can request a refund of deferrals within first 90 days ✓ Requires employer contributions (i.e. Safe Harbor) ✓ Requires annual increase in employee contribution rate up to at least 6% (i.e. auto-escalation) ✓ Auto-enrolled, but at how much? With auto-enroll plans, you pick your employees’ default contribution rate. This begs the question: how high should you set it? A default contribution rate of 3 percent used to be the most common, but that changed recently. According to The Plan Sponsor Council of America’s 64th Annual Survey, a 6 percent rate became the most popular in 2020. And if it helps any in your decision-making, our own data shows no evidence of higher default contribution rates leading to higher numbers of opt-outs. In addition to the default contribution rate, you’re also responsible for selecting the default investments for employees’ deferrals. This is what’s referred to as a Qualified Default Investment Alternative (QDIA)—and it can help limit your investment liability. Betterment at Work covers this base for all our 401(k) clients by defaulting employee deferrals into our Core portfolio, which meets QDIA criteria for transferability and safety. One potential downside of auto-enroll Making it easier for people to invest and save for retirement is a good thing. It’s sorta our thing. And if you have a Traditional 401(k) plan, an increased participation rate makes it more likely that your plan will pass the required compliance tests. However, there’s one downside to consider, and it’s mostly a matter of perspective. If you set your default contribution rate relatively low—let’s say less than 6 percent—and don’t actively encourage employees to bump that up as much as they can, they may not get on track to retire by their desired age. Is it better than saving nothing for retirement? Absolutely. But because employees didn’t actively choose the rate, they may not be inclined to increase it on their own. Wondering how to combat this retirement saving inertia? Well, it can be partially addressed by the aforementioned auto-escalation, which steadily increases employees’ contribution rates each year. We also help by offering your employees personalized retirement advice that helps keep them on track. How Betterment at Work makes ‘auto’ even easier As a digital 401(k) plan provider, we can help your employees save for their futures with compelling plan design features like auto-enroll. Our intuitive tech and committed service also lightens your administration load in the process. And let’s not forget about auto-escalation, which we offer at no added cost to new plans. Let us handle the work of monitoring who gets escalated. If your payroll provider is one we offer 360-degree integrations with, we'll even implement the increase ourselves. Last but certainly not least, we guide your employees through their contribution rates, investment options, and more. Even if your employees were auto-enrolled in the plan, they’ll get the encouragement they need to keep moving closer to retirement. -

![]()

Understanding 401(k) Nondiscrimination Testing